Last month in our blog post about using Xero and Wagepoint to assess whether our clients qualified for various Canadian subsidies, we mentioned that we would add to this topic by discussing how to record and bookkeep the subsidies received so that your financial statements are accurate.

It shouldn’t matter which accounting system you’re using since the accounting theory behind the transactions can be translated into most, if not all, accounting systems.

FYI:

- Sales tax (GST/HST, PST, RST) shouldn’t play a factor for any of the transactions below, aside from the last one (CECRA).

- We’ll be using the ‘cash method’ of accounting in the examples below.

THE CANADA EMERGENCY BUSINESS ACCOUNT (CEBA)

October 26, 2020 Update: CRA confirmed that the forgivable portion of the CEBA loan is taxable when received. The forgivable portion of the loan is included in income in the year in which the loan is received by virtue of Paragraph 12(1)(x). A taxpayer can elect under Subsection 12(2.2) not to include the forgivable amount in its income by reducing its outlay or expenses in respect of which the loan is received by the same amount. The election can be made by sending a signed letter to CRA by the due date for the corporate tax return covering the period in which the expenditure was made (note1). Amounts that are not forgiven can be deducted under Paragraph 20(1)(hh) for the year in which the repayment is made.

What is it?

A Government of Canada program that provides interest-free loans of up to $40,000 to small businesses. If the loan is repaid on or before December 31, 2022, 25% of the loan will be forgiven (i.e. $10,000). Therefore, only $30,000 of the $40,000 loan has to be repaid. The forgiven $10,000 is taxable income.

To determine eligibility, please read the program overview carefully. You can also refer to our previous blog post for more information.

How to record it

Step 1: Create a ‘Non-Current Liability’ chart of account (other ‘liability’ accounts work too)

- Use a simple naming convention so that you can keep track of the loan

- For example, name it ‘CEBA Loan’ or similar. You may want to include the name of the institution from where the funds were received in the chart of account name.

Step 2: When the funds are deposited into the business bank account, code them to this new account you just created

- This will be an increase (debit) to ‘Cash’ and a credit to your liability account

Step 3: Run a ‘Balance Sheet’ report to ensure the transaction was recorded correctly. You should see a $40,000 liability:

If you repay the loan after December 31, 2022, you will have to repay the full amount. Once that happens, the repayment will offset this account and the remaining balance will be $0.

Any interest paid to an institution after December 31, 2022 will be an interest expense, similar to any other loan.

Important: If you repay the loan prior to December 31, 2022, part of this loan is forgiven (as we mentioned above) and is taxable.

For example, if you repay $30,000 of the $40,000 on December 31, 2022, the remaining $10,000 is forgiven. Your liability account will now show $10,000 remaining even though it has been forgiven.

Our suggestion is to create an ‘Other Income’ account named ‘CEBA Loan Forgiveness’ or similar in your chart of accounts.

You’ll have to create a journal entry removing the $10,000 from the liability account to the ‘Other Income’ account:

Debit CEBA TD Bank Loan $10,000 (liability account)

Credit CEBA Loan Forgiveness $10,000 (other income account)

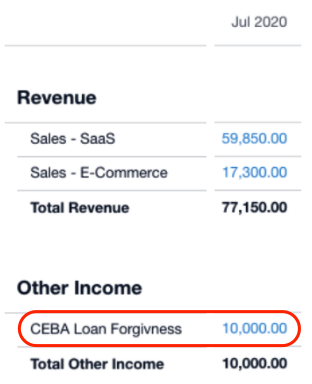

If you run a ‘Balance Sheet’ report, your ‘CEBA’ liability account should be $0.

If you run a ‘Profit and Loss’ (Income Statement) report, your ‘CEBA Loan Forgiveness’ income account should show $10,000.

THE CANADA EMERGENCY WAGE SUBSIDY (CEWS)

What is it?

A Government of Canada program that provides affected businesses and eligible employers with a subsidy of up to 75% of employee wages. As of July 17, 2020, the government announced changes that would continue the subsidy until December 19, 2020. Businesses have to show a drop in revenue to qualify.

To determine eligibility, please read the program overview carefully. You can also refer to our previous blog post for more information.

How to record it

Step 1: Create an ‘Other Income’ chart of account

- Use a simple naming convention so that you can keep track of the subsidy

- For example, name it ‘CEWS Subsidy’ or similar

Step 2: When the funds are deposited into the business bank account, code them to this new account you just created

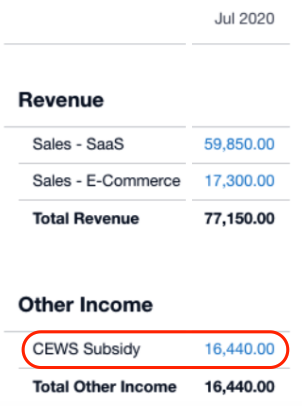

Step 3: Run a ‘Profit and Loss’ (Income Statement) report to ensure the transaction was recorded accurately:

THE 10% TEMPORARY WAGE SUBSIDY

What is it?

A Government of Canada program that allows eligible employers to reduce their payroll deductions required to be remitted to the Canada Revenue Agency (CRA). The subsidy is equal to 10% of the remuneration paid from March 18, 2020 to June 19, 2020, up to $1,375 per eligible employee to a maximum of $25,000 total per employer.

To determine eligibility, please read the program overview carefully. You can also refer to our previous blog post for more information.

How to record it

*Depending on your accounting system and payroll provider, there will be various ways to arrive at the final result*

Step 1: Create an ‘Other Income’ chart of account

- Use a simple naming convention so that you can keep track of the subsidy

- For example, name it ‘Temp Wage Subsidy’ or similar

Step 2: You’ll have to crunch the numbers to determine what your reduction in source deductions are for a certain period. Or if you use a payroll provider/system that has integrated the ‘10% Temporary Wage Subsidy’ computation into their platform, the calculation will be done for you.

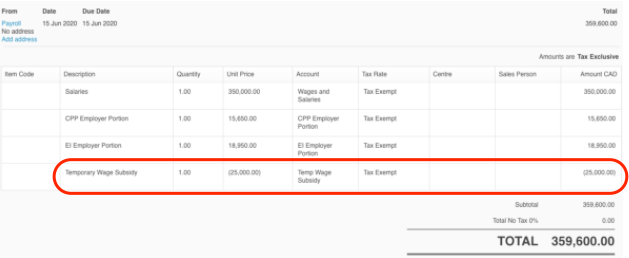

Step 3: Our suggestion is to record your payroll entries and the corresponding deductions as they would have been recorded had you not received the ‘10% Temporary Wage Subsidy’.

Step 4: You’ll have to, through either a journal entry, or an amendment to your payroll transaction, record the reduction in source deductions as ‘Other Income’ to the account created in ‘Step 1’ above.

- For example, you could enter the full payroll transaction in your accounting system and then enter a deduction on the last line (recorded to ‘Other Income’ > ‘Temp Wage Subsidy’) to reduce the transaction total (allowing it to reconcile to your bank statement transaction). This has the effect of creating a ‘credit’ and increasing the ‘Other Income’ account:

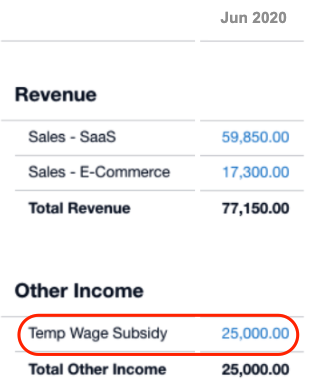

Step 5: Run a ‘Profit and Loss’ (Income Statement) report to ensure the transaction was recorded accurately.

CANADIAN EMERGENCY COMMERCIAL ASSISTANCE PROGRAM (CECRA)

What is it?

A Government of Canada program that provides affected businesses with rent relief of 75% - whereby the Government of Canada and the landlord cover 75% of the rent payment and the tenant covers 25% of the rent payment. The program is eligible for April, May, June and July and businesses have had to have steep revenue declines (70%).

To determine eligibility, please read the program overview carefully.

How to record it

*This will depend on whether you received a refund of rent already paid for the corresponding months or whether you receive a future rent credit. In addition, there are sales tax implications and some rent (25% most likely) has to still be recorded*

If you receive a refund of rent already paid

Step 1: Create an ‘Other Income’ chart of account

- Use a simple naming convention so that you can keep track of the subsidy.

- For example, name it ‘CECRA Subsidy’ or similar.

Step 2: When the funds are deposited into the business bank account, code them to this new account you just created.

Step 3: Run a ‘Profit and Loss’ (Income Statement) report to ensure the transaction was recorded accurately.

If you receive a credit for next month’s rent

If you paid rent and the landlord was providing you with a rent credit for subsequent months, then again, you would follow the flow funds from the bank statement. Rent expense would be recorded when paid and for the subsequent month, you would show no rent expense (since the month, in essence, is rent-free).

For the CECRA subsidy, you may have a combination of the above (i.e. rent paid and a refund or credit all in one month). You’ll have to just break it down and record each transaction separately and you should arrive at the desired result.

Good luck on your bookkeeping journey!

Feel free to add comments below and we can try to respond with some answers and insights.