Somewhere between $2M and $10M in revenue, most business owners have the same uncomfortable realization at least once: Something in the books from a year or two ago (or even longer) doesn't hold up.

Maybe a new accountant flagged it during onboarding. Maybe you switched accounting systems, and the migration surfaced GST/HST that was never remitted. Maybe you finally read your own financials closely enough to notice that the numbers do not reconcile with what you filed.

Whatever the trigger, you know something the CRA does not - at least not yet. You now have an urgent decision to make.

The instinct for most owners is to do nothing - to assume the odds of getting caught are low, and the cost of raising your hand is high. That instinct is usually wrong, and it became more wrong on October 1, 2025, when the CRA overhauled the program built for exactly this situation: the Voluntary Disclosures Program (VDP).

This is a working guide to that program: what it is, the five conditions you must meet, the two paths through it, and examples in which the VDP is clearly the right approach. The goal is to give you and your leadership team enough of a framework to know which situation you're in before you call anyone.

One note before we start: this is general information current as of May 2026, and does not constitute tax advice for your specific situation. Tax facts are specific, and the right answer depends on your particular set of facts. So please seek professional opinion before acting on any of this.

What is the VDP?

The VDP is the CRA's mechanism for allowing taxpayers to correct errors or omissions in past filings before the CRA discovers them. It is not a tax amnesty: You still pay every dollar of tax you owe. However, if CRA accepts your application, they may grant you three important items: relief from penalties, relief from a portion of the interest, and protection from criminal prosecution on the issue you disclosed.

The third item matters more than founders usually realize. Serious or sustained non-compliance - for example, years of unremitted GST/HST, or large amounts of unreported income - can become a prosecution problem. The VDP takes that off the table for the specific issue you bring forward.

The program covers most of what a Canadian business can get wrong, such as unfiled tax returns or information returns, unreported income, ineligible expenses claimed, unremitted source deductions (CPP and EI), and GST/HST not charged, collected, or reported. As of the October 2025 update, it also extends to newer regimes such as the Underused Housing Tax and the luxury tax.

If the problem is GST/HST specifically (and for a lot of fast-growing businesses, it is), it helps to understand how those obligations sneak up in the first place. We wrote about that in Canadian Sales Tax Rules Business Owners Learn Too Late.

Why is this more relevant than it was a year ago?

The reason to pay attention right now is that the program changed materially on October 1, 2025, and the changes generally run in the taxpayer's favour. Indeed, the CRA's stated goal was to make the VDP easier to access and easier to understand.

The old framework (set in 2018) sorted applications into a "General Program" and a "Limited Program," and the Limited Program was deliberately stingy with respect to penalty and interest relief. It also disqualified you the moment the CRA had made almost any kind of contact about the issue.

The new framework, set out in Information Circular IC00-1R7 for income tax and GST/HST Memorandum 16-5-1 for GST/HST, does three things that matter to a business owner:

It relaxes who qualifies.

Prior CRA inquiries, requests for missing returns, or general "education letters" no longer automatically disqualify you. However, you remain disqualified for the VDP if you are under audit or investigation on the issue, or you have been egregiously non-compliant.

It increases the relief.

The old VDP framework granted 100% penalty relief under the General Program, but penalties generally applied in full under the Limited Program. (Only gross negligence penalties were waived under the Limited Program) The new framework grants 100% penalty relief if “Unprompted” and up to 100% penalty relief if “Prompted”. (See below discussion on “Unprompted” vs. “Prompted”)

Furthermore, the old VDP framework generally granted a maximum of 50% of interest on amounts for years older than the three most recent years under the General Program, and no interest relief under the Limited Program. The new framework grants 75% relief of applicable interest if “Unprompted” and 25% relief if “Prompted”.

It simplifies the paperwork.

The new VDP regime offers a redesigned Form RC199, clarification of documentation requirements, and an easier path to a second application if you ever need one.

Here is the practical implication: most owners (and, candidly, some accountants) are still operating on the pre-2025 mental model, where the program was narrower and less generous. If someone told you two years ago that voluntary disclosure "wasn't worth it" for your situation, that assessment may simply be out of date.

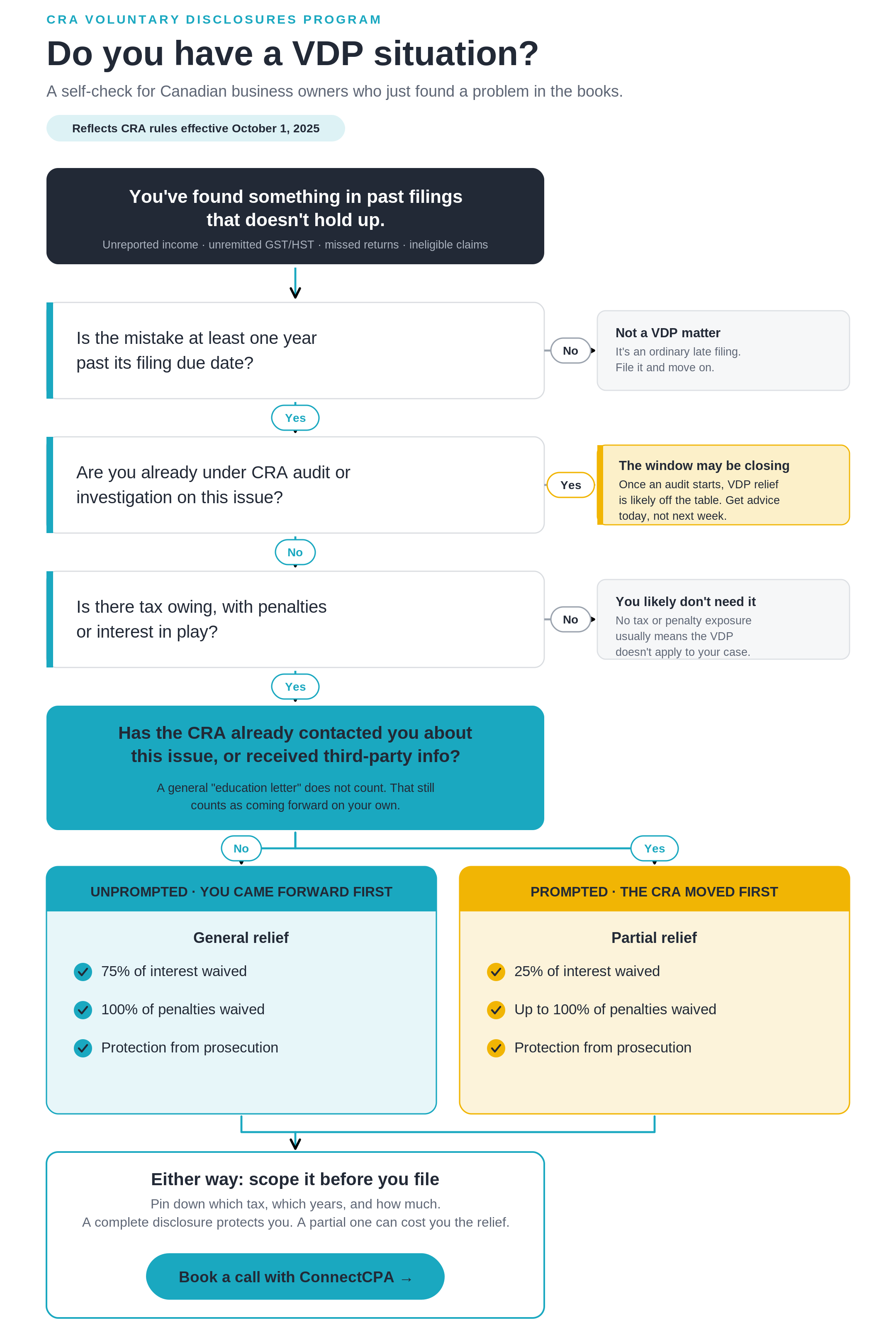

The five conditions for a valid disclosure

To get relief, your application has to satisfy all five of these. Miss one, and the application fails.

- It has to be voluntary. You must come forward before an audit or investigation has been initiated against you, or a related taxpayer, about the information you're disclosing. (Note the 2025 relaxation: a general education letter or routine CRA inquiry no longer automatically burns this condition.)

- It has to be complete. You must fully disclose the issue, with all the relevant information and documentation for the required years. A partial disclosure is not a smaller version of a valid one; it is simply invalid.

- There has to be a penalty in play. The issue being disclosed must carry applicable penalties. If there is no penalty exposure, you are not qualified for the VDP.

- It must be at least a year old. The information must be at least one year past its filing due date. You cannot use the VDP to clean up a return that happens to be a few months late. That is an ordinary late filing, which is handled in a different way.

- You have to pay, or arrange a payment. The application has to include payment of the estimated tax owing or a request for a payment arrangement (which is subject to CRA approval).

The two paths: Unprompted vs. Prompted (and why the difference is real money)

This is the part of the 2025 overhaul worth understanding before you do anything, because it is the part where speed translates directly into dollars.

The CRA now sorts every application into one of two categories, and the category determines how much relief you get.

“Unprompted”

This means that you are coming forward before the CRA has communicated with you about the specific issue. A general "education letter" - guidance, not a demand - still counts as “unprompted”. As noted above, unprompted applications generally receive 100% penalty relief and 75% interest relief.

“Prompted”

This means you are coming forward after the CRA has already contacted you about an identified issue - for example, a letter naming a specific error on your account, or setting a deadline to fix something. Alternatively, the CRA may have already received information about you from a third-party source. Prompted applications generally receive up to 100% penalty relief and 25% interest relief.

Both paths give you the same two things on top of the interest and penalty relief: protection from criminal prosecution, and no gross negligence penalties on the disclosed issue.

The gap between 75% and 25% interest relief is a key argument for moving quickly. On a tax balance that has been compounding daily for multiple years, that 50 percentage point swing in interest relief is frequently a five-figure number. Same problem, same person - the difference is whether they came forward before or after the CRA's letter landed.

Four scenarios: when it's clearly right, and when it isn't

Frameworks are easier to apply to concrete situations. Here are four, drawn from the patterns that actually show up in growing Canadian businesses.

Scenario 1: The multi-year GST/HST gap

A SaaS company grows from $400K to $2.8M over three years, selling to a mix of Canadian and US customers. Somewhere in year one, it blew past the $30,000 small-supplier threshold and should have registered for GST/HST, but nobody did until a new accountant caught it in year three. That's roughly two and a half years of GST/HST that should have been charged and remitted on the Canadian sales: call it $95,000 of tax, plus failure-to-file and failure-to-remit penalties, plus interest compounding the entire time.

No audit. No CRA letter. This is generally an unprompted application. Through the VDP, the $95,000 of tax is still owed (that part never changes), but the CRA may waive all penalties and 75% of the interest. On a balance that's been growing for nearly three years, the interest relief alone is usually well into five figures. And a sustained GST/HST collection failure of that size is exactly the kind of thing that can escalate past "balance owing." The VDP closes that door. Verdict: Clear VDP candidate. Move while it's still unprompted.

Scenario 2: Unreported foreign income and a missed T1135

A founder has a US-domiciled brokerage account, or income from a venture south of the border, that was never reported in Canada, and the T1135 “Foreign Income Verification Statement” was never filed. The T1135 penalty is punishing: $25 a day, up to $2,500 per year, before you even reach the tax on the unreported income or the gross negligence exposure on top of it.

This is a textbook VDP case, with one wrinkle. Foreign-sourced issues carry a 10-year documentation window, versus six years for Canadian-sourced income. The lookback is longer, and the paperwork is heavier, but the relief is correspondingly larger, and the prosecution protection on unreported offshore income is not optional peace of mind; rather, it is the whole point. There's also a timing risk: the CRA increasingly receives this information automatically through information-sharing agreements with other countries. If that data lands before you come forward, you've flipped from unprompted to prompted. Verdict: Clear VDP candidate. The foreign element makes the clock more urgent, not less.

Scenario 3: The education letter

A founder receives a letter from the CRA. It doesn't name a specific error on their account. It doesn't set a deadline. It's general guidance - "businesses in your sector commonly misunderstand X; here's how the rule actually works." That's an education letter, and under the 2025 rules, receiving one does not cost you unprompted status.

This is the scenario where speed is everything. The founder who recognizes that the letter describes a real problem and quickly files a complete VDP application generally still qualifies for full penalty relief and 75% interest relief. The founder who sits on it until the CRA follows up with a letter naming their specific account has, in that interval, downgraded themselves to up to 100% penalty relief and 25% interest relief. Same problem, same person, materially worse outcome - decided entirely by how fast they moved. Verdict: Clear VDP candidate, and the one where the delay is most expensive.

Scenario 4: The debatable expense

Not every "this might be wrong" is a VDP situation. Consider a founder whose company claimed a home-office allocation, a vehicle expense, or a meals-and-entertainment classification that is aggressive but defensible - a genuine interpretation question, not an omission. The dollar amount is modest, the position is arguable, and there was a reasonable basis for what was filed.

Filing a VDP application here is usually the wrong move. The program is built for clear errors and omissions - unreported income, unremitted tax - not for re-litigating judgment calls the CRA might never question and that you might well win if they did. Disclosing a debatable position does not buy you protection; rather, it invites scrutiny of a return that was, on balance, fine. Verdict: Not a VDP case. The VDP is for the things you know are wrong. It is not a tool for managing anxiety about the things that are merely arguable.

How to apply: the actual steps

If you have worked through the framework and are looking at a real disclosure, here is what the process involves.

Step 1 - Scope the full problem.

Before anything is submitted, you (or your advisor) need the complete picture: which tax, which years, how much. The "complete" condition is not a formality.

Step 2 - Consider a pre-disclosure discussion.

The CRA runs an anonymous, informal, non-binding pre-disclosure discussion service. You can talk through your situation without revealing your identity, to understand the process, the risks of staying non-compliant, and the relief likely available - before you commit. It doesn't guarantee anything and it doesn't stop the CRA from acting, but it lets you assess from behind the curtain. It's accessed through the CRA's general enquiries lines.

Step 3 - Assemble the documentation.

That means the completed and signed Form RC199, Voluntary Disclosures Program Application - the redesigned version released in October 2025, and now mandatory - plus all the returns, forms, and schedules needed to correct the non-compliance. The documentation windows are: the last 10 years for foreign-sourced income or assets, the last 6 years for Canadian-sourced income or assets, and the last 4 years for GST/HST issues.

Step 4 - Include the payment.

Payment of the estimated tax owing, or a formal request for a payment arrangement.

Step 5 - Submit through one channel only.

Online through CRA My Account, My Business Account, or Represent a Client; by fax; or by mail to the VDP office in Shawinigan, Quebec. Pick one - do not duplicate.

Step 6 - Get your effective date.

The CRA sends an acknowledgement letter confirming the effective date of disclosure - the date your complete application was received. That date is what locks in your "voluntary" status. It's the single clearest reason a complete application filed sooner beats a perfect application filed later.

A representative (your accountant) can submit on your behalf, but both you and the representative have to sign, and the representative has to be authorized with the CRA.

Why most accountants don't bring this up

It is worth being direct about the question in the title. The program is not obscure: It is on the CRA's website, it is thoroughly documented, and tax professionals know that it exists.

There are two real reasons it does not come up, and neither is comfortable.

The first is that the calculus is genuinely hard. A VDP recommendation requires an advisor to assess detection risk, quantify multi-year exposure, make a judgment call about prosecution risk, and then put that recommendation in writing, with their name on it. In the short term, it may be easier for them to simply not raise it.

The second is more uncomfortable. Surfacing a past problem sometimes means surfacing a problem that happened on the accountant's or bookkeeper's own watch. A firm that missed a GST/HST registration threshold for two years is not enthusiastic about being the one to point it out. The incentive to let a sleeping problem lie is real - and it is not aligned with yours.

That is likely the honest answer. The reason the VDP does not come up is that raising it requires the kind of conversation that some accountants would rather avoid. It is the same dynamic that lets documentation gaps quietly widen until they turn into a CRA problem - something we covered in CRA Audit Red Flags: How Documentation Gaps Escalate CRA Reviews.

FAQ: The VDP and your accountant

Can my accountant file a VDP application for me?

Yes. A representative can submit on your behalf, but both you and the representative must sign the application, and the representative must be authorized with the CRA before they can act for you.

Will applying for the VDP trigger an audit?

A VDP application is not itself an audit. The point of the program is to resolve the disclosed issue outside of an audit. What does raise audit risk is an incomplete or sloppy application, which is the strongest argument for scoping the full problem before you file anything.

How long does the process take?

It varies, and the CRA reviews each application on a case-by-case basis. A clean, single-issue disclosure moves faster than a complex multi-year one. Plan for months, not weeks, and note that your effective date of disclosure (and therefore your "voluntary" status) is locked in when the complete application is received, not when it's resolved.

Does the VDP cover my whole business, or just the issue I disclose?

Only the issue you disclose. The relief and the prosecution protection apply to the specific non-compliance in your application - not to anything else in your filing history.

Can I use the VDP more than once?

It's designed to be used once. Since October 2025, the CRA may consider a second application if it relates to a genuinely different matter, or if the circumstances behind it were beyond your control.

What does the VDP not cover?

It is not for returns that result in a refund or no tax owing. It is not for increasing input tax credits or other credits without a corresponding increase in tax liability. It cannot be used to make or change an election. And it cannot get you relief on penalties or interest that have already been assessed - once the CRA has assessed it, that window is closed.

The bottom line

A past problem in your books has a shelf life. Right now, before a CRA letter, before a third-party report lands, while you still qualify as unprompted, you have the most options and the best relief available. That window closes quietly. It does not announce itself.

If something in this guide describes a situation you recognize, the next step is not to file anything blindly. Rather, it is to properly scope it - figure out exactly which tax, which years, and how much, so you know whether you are looking at a clear VDP case.

That's a conversation worth having before the decision gets made for you. Book a call, and our team will help you work out what the right move is from here.