Ask any business owner what keeps them up at night, and cash flow is almost always in the top three. The uncomfortable truth most founders don't want to hear: cash flow problems are usually bookkeeping problems.

You can't fix what you can't see. If your books are three months behind, miscategorized, or living in a shoebox of receipts, you're not running a business. You're guessing at one.

The good news? Bookkeeping isn't complicated. It's just consistent. This guide walks you through exactly what bookkeeping is, what it isn't, what Canadian small business owners actually need to track, and how to build a system that grows with you instead of collapsing under it. No accounting degree required.

What is bookkeeping, really?

Bookkeeping is the ongoing practice of recording every dollar that moves in or out of your business, including sales, expenses, transfers, payroll, and taxes, in a way that's accurate, organized, and easy to pull up when you or the CRA need it.

That's it. No mystery.

What often confuses owners is the overlap with accounting. The distinction is simple:

- Bookkeeping captures and organizes the data.

- Accounting interprets that data to guide decisions, strategy, and compliance.

Think of bookkeeping as the foundation of a house. Accounting is the architecture built on top. If the foundation is crooked, everything above it cracks. This is why a brilliant accountant working with sloppy books can still give you bad advice. The input data is wrong.

For a closer look at where bookkeeping ends and higher-level financial oversight begins, our post on the difference between a bookkeeper and a controller is worth reading alongside this one.

Why clean books matter more than you think

Most small business owners think of bookkeeping as a compliance chore. It's actually three things at once.

A legal requirement. The CRA requires you to keep adequate records for six years from the end of the last tax year they relate to. If you're audited and your records are incomplete, Input Tax Credits can be denied even for legitimate expenses.

A decision-making tool. Clean books tell you which clients are profitable, which services are bleeding you dry, and whether you can actually afford that new hire.

A valuation asset. If you ever sell, raise capital, or bring in a partner, the first thing anyone looks at is your books. Disorganized financials can knock 15 to 30 percent off a business valuation, and in some cases kill the deal entirely.

Put simply, bookkeeping is one of the clearest decision-making tools your business has, and most owners aren't using it that way.

What Canadian small businesses need to track

The bookkeeping world loves to throw around terms like "chart of accounts" and "general ledger," but let's cut through it. Here's what you actually need to capture, organized in a way that reflects how Canadian businesses really operate.

1. Revenue (income)

Every dollar earned, whether from sales, services, retainers, commissions, or any other source. Track this by revenue stream, not as one lump sum. If you run a consultancy with three service lines, you need to know which one is pulling its weight and which one is quietly underperforming.

2. Expenses

Money flowing out. The mistake most owners make is lumping everything into "office supplies" or "miscellaneous." Resist the urge. Clean expense categorization, covering rent, software subscriptions, professional fees, marketing, meals (note that meals and entertainment are only 50% deductible in Canada), travel, and insurance, is what makes your financial reports useful when you actually need them.

3. Payroll and contractor payments

Keep this strictly separate from general expenses. Wages, CPP, EI, employer health tax (where applicable), and contractor payments all have their own reporting and remittance obligations. Mixing payroll into your general expense buckets is one of the fastest ways to create problems at year-end. Contractor payments, in particular, fall into T4A territory, with their own filing requirements. For a breakdown of the most common payroll errors we see, this post is a good starting point.

4. GST/HST collected and paid

If your taxable revenue has crossed, or is approaching, $30,000 over any four consecutive calendar quarters, you're required to register for GST/HST and start collecting it. The CRA gives you 29 days after crossing the threshold to register. Your books need to cleanly separate:

- GST/HST collected on sales (money you owe the government)

- GST/HST paid on eligible expenses (money you can claim back as Input Tax Credits)

Getting this wrong is one of the most expensive bookkeeping errors we see. If you want a list of best practices for sales tax before setting it up in your books, start there.

5. Bank and credit card transactions

Every deposit, withdrawal, transfer, and charge across all business accounts. These are the raw source data your books reconcile against. If your bookkeeping doesn't match your bank statement at the end of every month, something is wrong. Every time. Understanding why bank reconciliation matters is worth five minutes if you've never thought much about it.

6. Source documents

Receipts, invoices, contracts, vendor bills, expense reports. The CRA requires these to support every entry in your books. Digital copies are accepted and, in practice, much easier to manage than paper. "Adequate records" means legible, organized, and retrievable on demand.

How long do you need to keep it all?

The rule most Canadian business owners get wrong: the CRA requires you to keep business records for six years from the end of the last tax year they relate to, not six years from the date of the receipt.

So if you're filing for the 2024 tax year, you're holding those records until at least the end of 2030. Longer if you're under appeal, own capital property, or have ever been late filing.

A few practical exceptions:

- Dissolved corporations: two years after dissolution

- Property records: until six years after you dispose of the property

- Unfiled or fraudulent returns: indefinitely

Digital records count, and are almost always easier to manage than physical ones. Just make sure they're backed up and accessible.

Cash vs. accrual: the one decision that shapes everything

Before you set up a single account, you need to pick a method: cash-basis or accrual-basis bookkeeping. This isn't a throwaway decision. It shapes what your reports actually tell you.

Cash-basis

You record income when money hits your account, and expenses when money leaves it. Simple, intuitive, and fine for very small operations or freelancers.

The catch is that it can hide problems. If you invoice a client $20,000 in December but they don't pay until February, cash-basis shows December as a dead month. Your profit looks terrible. You make decisions based on a picture that isn't accurate.

Accrual-basis

You record income when it's earned and expenses when they're incurred, regardless of when money actually moves. This matches revenue to the period it belongs to, which gives you a much truer picture of performance.

The catch here is that it requires more discipline and better systems, but it's the only method that scales.

Which should you pick?

For most Canadian businesses beyond the very early stage, and definitely any business approaching or above the $30,000 GST/HST threshold, accrual is the right default. The CRA generally expects accrual accounting for businesses, with narrow exceptions for certain farming, fishing, and commission-based income. If you're growing, plan to hire, or ever want to understand your real profitability, start on accrual.

Switching later is possible but painful. Start the way you mean to continue. If you want to go deeper on this decision, our post on how your accounting method impacts everything covers it thoroughly.

Building a bookkeeping system that works

This is where most small business owners either over-engineer or under-build. The right system is the one that fits where you are right now and has room to grow. Here's a stage-by-stage approach.

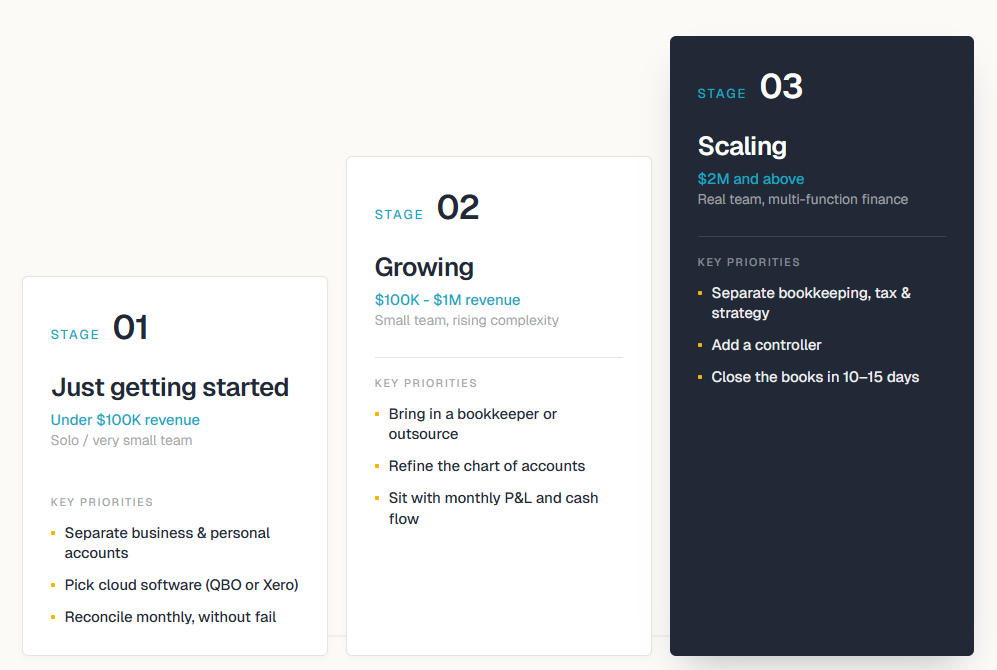

Stage 1: Just getting started (under $100K revenue, solo or very small team)

Your priorities at this stage are separation, consistency, and simplicity.

Open a dedicated business bank account and credit card before anything else. Mixing personal and business finances is the single most common, and most expensive, early mistake you can make. Once that line is blurred, it's time-consuming and costly to untangle.

Pick cloud accounting software. QuickBooks Online and Xero are the two most widely used options in Canada. Both integrate cleanly with Canadian banks, handle GST/HST, and connect to payroll tools. Avoid spreadsheets past your first few months. They break down faster than you'd expect.

Set up a basic chart of accounts. Your accountant or bookkeeper can do this in an afternoon. Don't overthink it at this stage.

Reconcile monthly. Matching every transaction in your books to your bank statement is one habit that catches the majority of errors before they compound.

Stage 2: Growing ($100K to $1M revenue, small team)

Your priorities shift here toward accuracy, categorization, and insight.

Bring in a bookkeeper, or outsource that function. At this stage, your time is genuinely better spent on revenue-generating work. A skilled bookkeeper pays for themselves through found deductions, cleaner reports, and hours you get back. If you're on the fence about whether it makes sense, our post on why businesses outsource bookkeeping walks through the practical considerations.

Get serious about your chart of accounts. Refine categories so your profit and loss statement actually tells you which parts of the business are thriving and which aren't.

Consider separating your operating accounts. Many growing businesses use a structure along the lines of Profit First, with separate accounts for taxes, payroll, operating expenses, and owner pay. It's not mandatory, but it builds financial discipline into the structure of your accounts rather than relying on willpower alone.

Review monthly reports. Not just scan them. Actually sit with them. Your bookkeeper or accountant should walk you through the P&L, balance sheet, and cash flow statement every month. If you're not sure which reports matter most, our breakdown of which financial reports to review monthly is a useful starting point.

Stage 3: Scaling ($2M and above, real team, more complex operations)

Your priorities here are controls, strategy, and systemization.

Separate the functions. Bookkeeping, tax filing, and financial strategy should not all sit with the same person. You want checks and balances, and you want each role filled by someone whose job it is to own that piece.

Consider outsourced controller or fractional support. A bookkeeper records what happened. A controller ensures the books are clean, compliant, and audit-ready. These roles matter at this stage, and most companies don't need them all full-time. The value of fractional controllership is worth understanding if you're not familiar with how that model works.

Build a month-end close process. A documented, repeatable checklist that closes the books within 10 to 15 business days of month-end is one of the clearest markers of a finance function that actually works.

Track the metrics that matter for your model. Gross margin by service line, customer acquisition cost, lifetime value, revenue per employee, days sales outstanding. Your books should feed these numbers. If they can't, the system needs work.

Your bookkeeping rhythm: weekly, monthly, quarterly, annually

Bookkeeping breaks down when it becomes one massive task you do once a year in a panic. Treat it as a rhythm instead, and the time involved shrinks considerably.

Weekly (15 to 30 minutes)

Send invoices for completed work. Review and categorize any transactions your software didn't auto-sort. File or upload receipts. Follow up on anything overdue.

Monthly (2 to 4 hours, or your bookkeeper's time)

Reconcile every account against bank and credit card statements. Review the profit and loss statement and balance sheet and look at variances from previous months. Process payroll and remit source deductions. Review accounts receivable and payable aging. We have a monthly bookkeeping checklist you can work from directly if you want something structured.

Quarterly (varies)

File GST/HST returns if you're on a quarterly filing schedule. Businesses under $1.5M typically file annually, $1.5M to $6M file quarterly, and over $6M file monthly. Remit corporate tax installments if required. Review budget versus actual performance. Assess your cash flow runway.

Annually

Close out the year and prepare your financial statements for your accountant. File corporate or self-employment taxes. Issue T4s for employees and T4As for contractors. Review pricing, compensation, and financial structure for the year ahead.

The businesses that stay on top of this aren't necessarily the most disciplined ones. They're the ones with the best systems, where software, automation, and a clear division of responsibility take the friction out of the process.

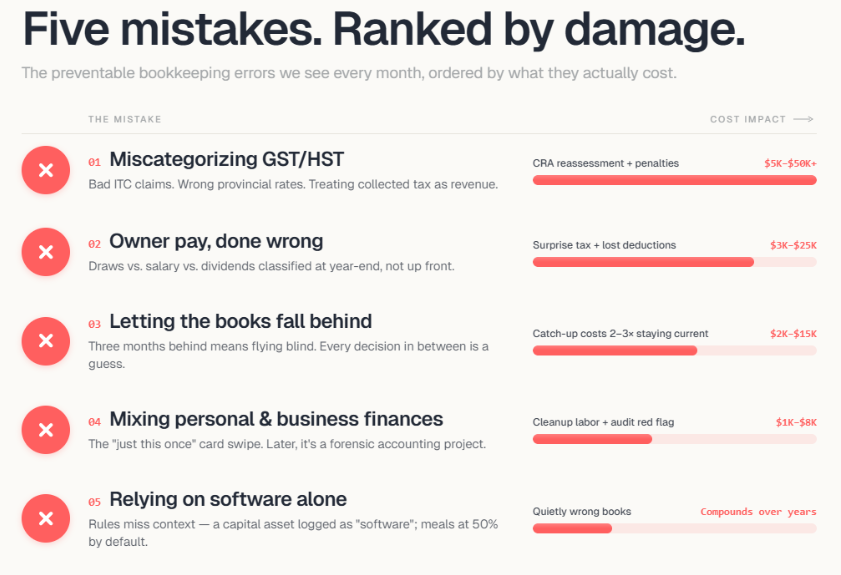

The five most expensive bookkeeping mistakes we see

Every month we come across the same preventable errors. Here are the ones that cost the most. For a deeper look at patterns across all of them, our post on the five most common bookkeeping pitfalls is worth a read too.

1. Mixing personal and business finances

The founder puts groceries on the business card "just this once." Six months later, their books are a forensic accounting project. Clean separation from day one saves thousands in cleanup fees and removes a serious red flag if you're ever audited.

2. Miscategorizing GST/HST

Claiming Input Tax Credits on expenses that don't qualify. Forgetting to charge HST on invoices to Ontario clients while using GST-only rates for Alberta ones. Treating GST/HST collected as revenue. It's not yours to keep. It belongs to the CRA. Any one of these errors can trigger a reassessment, with penalties and interest that compound monthly. For a closer look at how documentation gaps tend to escalate CRA reviews, our article on CRA audit red flags is exactly on point.

3. Owner draws vs. salary vs. dividends, done wrong

For incorporated businesses, how you pay yourself carries significant tax implications. Many owners just take money out without classifying it properly. The result is surprise personal tax bills, lost deductions, and messy year-end cleanup. This needs to be set up correctly from the start, with your accountant's input. Our post on how to pay yourself as a Canadian business owner covers the key considerations.

4. Letting the books fall behind

A business that's three months behind on bookkeeping is essentially flying blind. Every decision you make during that period is a guess. Catch-up bookkeeping also costs two to three times more than staying current, both in fees and in deductions that get missed or mistimed.

5. Relying on software alone

Cloud accounting tools are powerful, but they categorize based on rules and patterns. They don't know that the $4,000 "software" charge was actually a capital asset, or that the $800 at a restaurant was a full-team offsite (fully deductible) rather than client entertainment (50% deductible). Software without human oversight produces confidently wrong books. Our post on why human-led accounting still wins in a tech-heavy world gets into exactly why that gap exists.

DIY, in-house, or outsourced: how to decide

There's no universal right answer here. There is, however, a point where doing it yourself stops making financial sense, and most business owners cross that line later than they should.

Quick test: what is your time worth per hour, and how much of it are you spending on bookkeeping? If your hourly value is $150 and you're spending eight hours a month on work a bookkeeper could handle for $400, you're losing money by doing it yourself.

When it's time to call in help

There are a few clear signals that you've outgrown your current setup.

You can't answer basic financial questions quickly. "What's our cash runway?" "Which service line is most profitable?" "Are we actually growing or just getting busier?" If these take hours or days to answer, your books aren't working.

Tax season is a fire drill. If you're still assembling records in April, something upstream is broken.

You're avoiding looking at your numbers. Procrastination here is almost always a signal that, somewhere, you already know something is off.

You've received a CRA notice or reassessment. Get professional support immediately.

You're planning to raise capital, sell, or bring on a partner. Your books need to be due-diligence-ready, and that usually means six to twelve months of cleanup if they aren't already.

The bottom line

Bookkeeping isn't the glamorous part of running a business, but it's the part that determines whether the glamorous parts ever happen.

Clean books give you clarity. Clarity gives you confidence. And confidence is what separates the owners who scale from the ones who stall.

Start with the basics: separate accounts, cloud software, monthly reconciliation. Build a rhythm. Know when to bring in help. And treat your books not as a tax obligation, but as the most honest feedback mechanism your business has.

Key takeaways

- Bookkeeping is the foundation. Accounting, strategy, and valuations are all built on top. If the foundation cracks, everything above it does too.

- Track six things well: revenue, expenses, payroll, GST/HST, bank activity, and source documents. Organized, categorized, consistent.

- Accrual beats cash for most growing businesses. It gives you a truer picture of performance and is what the CRA generally expects.

- Match your system to your stage. DIY at the start is fine. Past $100K to $250K, the math almost always favours outsourcing.

- The CRA wants six years of records. Digital is fine. Disorganized is not.

- Most bookkeeping disasters are preventable. Mixing accounts, GST/HST errors, falling behind, and unsupervised software are the usual culprits.

Frequently asked questions

Do I legally need to keep books if I'm a sole proprietor?

Yes. Anyone earning business or self-employment income in Canada is required to keep adequate records. The CRA doesn't care whether you're incorporated. They care that your records support every number on your tax return.

When do I need to register for GST/HST?

Once your taxable revenue exceeds $30,000 over any four consecutive calendar quarters (or within a single quarter), you have 29 days to register. Many businesses register voluntarily before that threshold to start claiming Input Tax Credits on startup expenses right away.

How often should I reconcile my books?

Monthly, at minimum. Weekly is better if your transaction volume is high. The longer you wait, the more errors compound and the harder they become to untangle.

Is QuickBooks or Xero better for Canadian businesses?

Both are excellent and widely used in Canada. QuickBooks has deeper market share and broader bookkeeper familiarity. Xero has a cleaner interface and handles multi-entity structures well. The best option is usually the one your bookkeeper or accountant already works in fluently. Ask them before you decide.

Can I switch from cash to accrual later?

Yes, but it requires notifying the CRA and typically involves an adjusting entry to bring prior-period accounts receivable and payable onto the books. It's cleaner to start on accrual if you anticipate growth. Switching later is doable; it's just more work than getting it right the first time.

What's the difference between a bookkeeper, accountant, and controller?

A bookkeeper records transactions. An accountant prepares financial statements, files taxes, and advises on compliance. A controller oversees the entire finance function, ensuring books are accurate, controls are in place, and reporting is reliable. Growing businesses eventually need all three, whether full-time or fractional.

If your books have outgrown your current system, or you're genuinely not sure whether they have, we'd be glad to take a look. ConnectCPA provides controllership and bookkeeping support for Canadian businesses that have moved past the DIY stage and need a partner who takes your numbers as seriously as you do. Book here for a complimentary call.