The question is almost always framed wrong. "Should we hire an accountant or outsource it?" treats finance as a binary choice between two boxes, and the binary answer almost never holds up in practice.

The better question is:

Which parts of your finance function belong in-house, which belong outside, and how do those two layers talk to each other?

That reframe matters because the binary answer breaks down quickly. A $3M services business that hires a full-time controller usually ends up overpaying for capacity they don't use. A $15M company running everything through an external firm usually ends up with delayed reporting and a CEO who can't get a quick answer on Friday afternoon. The companies that get this right almost always land somewhere in the middle, and they land there on purpose.

This guide walks through how internal and external accounting teams actually compare across the dimensions that matter, when each model starts to break, and how to think about building a finance function that grows with you instead of constantly being rebuilt.

Internal vs. External

Before getting into trade-offs, it helps to be precise about what each model looks like in a Canadian SMB context, because the terms get used loosely.

Internal (in-house) finance

A team member, or a small team, employed directly by your company. At the $2M to $10M revenue range, internal finance usually looks like one of three setups:

- A bookkeeper or accounting clerk (around $55K to $80K) handling AP, AR, payroll, and basic month-end.

- A controller ($90K to $150K) running the full close, building reports, managing compliance, and acting as the financial right-hand to the CEO.

- A director of finance or VP Finance ($140K to $220K+) for businesses approaching $20M or with real complexity (multi-entity, multi-currency, investor reporting).

- An external accountant to help with tax compliance and sales tax filings ($5K to $15K, or more, depending on complexity and nature of tax advice)

These are loaded costs. Add 20% to 30% for benefits, payroll taxes, software seats, training, and turnover risk.

External (outsourced) accounting

A firm or fractional resource that handles your finance function from outside the company. The mature version of this is not "we send receipts to a bookkeeper." It's a structured engagement that typically includes:

- Monthly bookkeeping and reconciliation

- Payroll administration

- GST/HST and corporate tax filing

- Monthly financial reporting (P&L, balance sheet, cash flow)

- Year-end close and tax preparation

- Advisory and ongoing CFO/controller-level oversight

The good firms operate as a true external finance department, with documented processes, defined deliverables, and a clear point of accountability. The weak ones operate like a freelance bookkeeper with a logo.

That distinction matters more than internal vs. external itself.

Where each model wins and loses

Here's where most "versus" posts go off the rails, listing surface-level pros and cons that don't survive contact with a real operating business. The dimensions that actually matter when you're choosing are these.

1. Cost

This is the dimension everyone leads with, and it's usually misunderstood.

A full-time in-house bookkeeper in a major Canadian market runs $70K to $90K all-in once you factor benefits, software, equipment, and the cost of recruiting and onboarding. A controller runs $115K to $180K all-in. That's a fixed cost, paid regardless of whether your transaction volume is up or down that month.

A well-scoped outsourced engagement for a $2M to $10M business typically runs $2,500 to $8,000 a month depending on complexity, which works out to $30K to $96K a year. That includes the team, the systems, the oversight, and the redundancy.

The honest read: at lower complexity, outsourced wins on cost decisively. At higher complexity and higher volume, the math gets closer, and internal can become competitive (especially when you factor in the value of having someone embedded full-time). But "cost" is rarely the actual decision driver once a business is past survival mode. Capability and reliability matter more.

2. Expertise depth and breadth

One in-house bookkeeper or controller is one person's experience, one person's judgment, one person's blind spots. They might be excellent at what they know and unfamiliar with what they don't.

An external firm gives you access to a team. Tax specialists, payroll specialists, technology specialists, advisory specialists. You're not paying for one brain. You're paying for a structured system with multiple brains behind it.

The trade-off: external teams are broader but less embedded. They don't know in their bones that the Tuesday morning review with your sales lead always runs over, or that your biggest client gets nervous when invoices arrive late in the month. Internal hires absorb that institutional context in a way external partners take longer to develop, and sometimes never fully do.

3. Availability and response time

This is where in-house finance has its clearest structural advantage. Walk down the hall, get an answer. Ping someone on Slack at 9 PM during a board prep, get a response.

External firms can be responsive, but they're never as immediately available as someone sitting in your office. The good ones set clear SLAs (response within four business hours, monthly close completed by day 10, etc.) and the great ones meet them consistently. But there's still a gap. If you're the kind of operator who needs ad-hoc finance answers throughout the day, that gap can feel frustrating.

The honest answer: most founders think they need this level of access more than they actually do. Once a structured reporting rhythm is in place, the "I need to know right now" moments drop dramatically.

4. Systems, controls, and process maturity

This is the dimension most owners underweight, and the one that has the biggest long-term impact.

A growing business needs a real finance system. Documented month-end close procedures. Reconciliation checklists. Approval workflows. Audit trails. Software stack decisions (which accounting platform, which payroll tool, which expense management, which AR automation).

External firms build this for a living. They've seen 50 versions of a month-end close and they know which ones break. Most in-house hires, especially first hires, are too busy doing the work to build the system. The result is a finance function that depends entirely on one person's habits, with no documentation and no backup.

If you ever fire that person, lose them to a competitor, or have them go on parental leave, you're rebuilding from scratch. We see this constantly during cleanup engagements.

5. Continuity and key-person risk

Related to the point above, but worth its own line. An in-house team of one is a single point of failure. If they leave, your books stop. Your tax filings stop. Your payroll might stop. The cleanup cost of a finance team member leaving without proper documentation routinely runs $10,000 to $30,000.

External firms have built-in redundancy. If your primary contact leaves the firm, the team continues. The processes are documented. The historical knowledge sits with the firm, not with one human being.

This is one of the most underestimated reasons businesses move from internal to external as they professionalize.

6. Strategic insight vs. transactional work

A bookkeeper records what happened. A controller ensures the record is accurate and reportable. A CFO tells you what to do next. These are different jobs, and the trap is hiring one and expecting all three.

Most internal hires at the $2M to $10M stage are mid-level. They do the work well, but they don't have CFO-level strategic experience, and they're not paid like someone who does. External engagements can layer in fractional CFO or advisory time at a fraction of the cost of a full-time hire, giving you access to senior thinking without the senior salary.

The risk on the external side: not every outsourced firm actually delivers strategic insight. Many are bookkeeping shops in a nicer wrapper. Vet carefully.

7. Confidentiality and control

A real consideration, often overstated. Some founders worry about an external team handling sensitive financial information, especially during fundraising or sale prep.

In practice, reputable Canadian accounting firms operate under professional confidentiality standards, with NDAs, secure portals, and structured access controls. The risk profile is generally lower than an in-house employee with a personal grievance and access to the books.

Where this concern is legitimate: founder-led businesses with highly sensitive owner compensation, related-party transactions, or strategic information that is genuinely confidential beyond standard NDA protection. Those situations sometimes warrant in-house control, or at least a carefully scoped external arrangement.

When each model breaks

Pros and cons in the abstract don't help anyone decide. What matters is recognizing the signs that your current model is failing you. Both models have predictable breaking points.

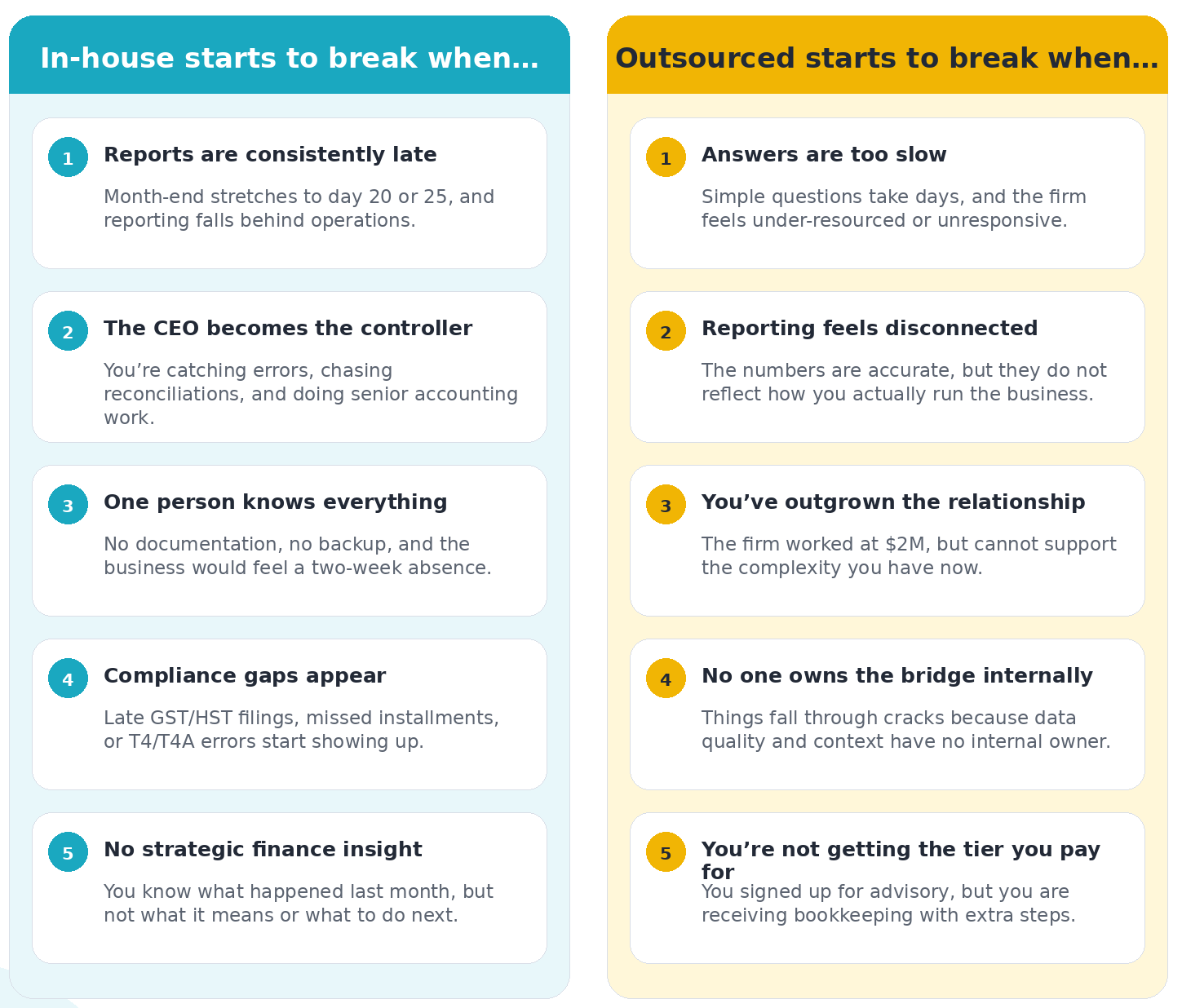

When in-house accounting teams start to break

- Reports are consistently late. Month-end stretches to day 20, then day 25. The team is buried in transactional work and never gets to reporting on time.

- The CEO is the de facto controller. You're the one catching errors, flagging weird transactions, and chasing reconciliation issues. That's a senior accounting role, not a CEO job.

- One person knows everything. No documentation. If they took two weeks off, the business would feel it.

- Compliance gaps are appearing. Late GST/HST filings, missed installments, T4/T4A errors. Usually a sign the in-house team is in over their head on scope.

- No strategic finance insight. You can see what happened last month but you can't answer what it means or what to do about it.

When external accounting teams start to break

- You can't get answers fast enough. Simple questions take days. Your external team is unresponsive or under-resourced.

- Reporting feels disconnected from operations. The numbers are accurate but they don't reflect how you actually run the business. No one's translating between operational reality and the financial story.

- You've outgrown the relationship. Your firm was great at $2M, but at $8M you need more sophistication than they can offer. The engagement hasn't scaled with you.

- There's no embedded ownership. Things fall through cracks because no one inside the company owns the relationship or the data quality.

- You're paying for a service tier you don't get. You signed up for advisory and you're getting bookkeeping with extra steps.

If you're seeing three or more signs on either list, your current setup isn't serving you anymore.

The hybrid model: what most $2M to $10M companies need

Here's what we see working most often in the Canadian SMB market, and it's not "fully internal" or "fully external." It's a deliberate layering of the two.

The typical structure

- An internal finance ops person. Could be a junior accountant, AR/AP coordinator, or finance operations associate. Sits inside the business, handles day-to-day tasks (invoicing, expense capture, vendor management, payroll inputs), and acts as the bridge to the external team. Loaded cost: $55K to $90K.

- An external accounting partner. Handles the structured monthly close, reporting, tax compliance, payroll administration, and advisory work. Brings the systems, the redundancy, the specialist depth, and the senior oversight.

This model gives you the speed and embedded context of internal, with the depth, systems, and continuity of external. It's also far more cost-effective than building a real internal finance team at this stage. A $90K coordinator plus a $5K/month external partner ($60K/year) gives you a $150K finance function that performs like a $250K+ in-house team, with built-in redundancy and senior advisory access.

When to evolve out of hybrid

The hybrid model has a natural ceiling. Around $15M to $25M, depending on complexity, most businesses graduate to an internal controller or director of finance, with the external firm shifting toward tax, audit support, advisory, and specialist work.

The key word is "evolve." Most failed transitions happen because owners try to internalize everything at once. Keeping the external partner during the transition (and beyond, in a narrower scope) is almost always the right move.

That being said, we’ve seen teams raise funds and build an internal accounting team early on and we work with clients that still prefer an external accounting and finance team beyond $50M in revenues.

A simple decision framework

Skip the generic flowchart. The real decision comes down to four questions, in order.

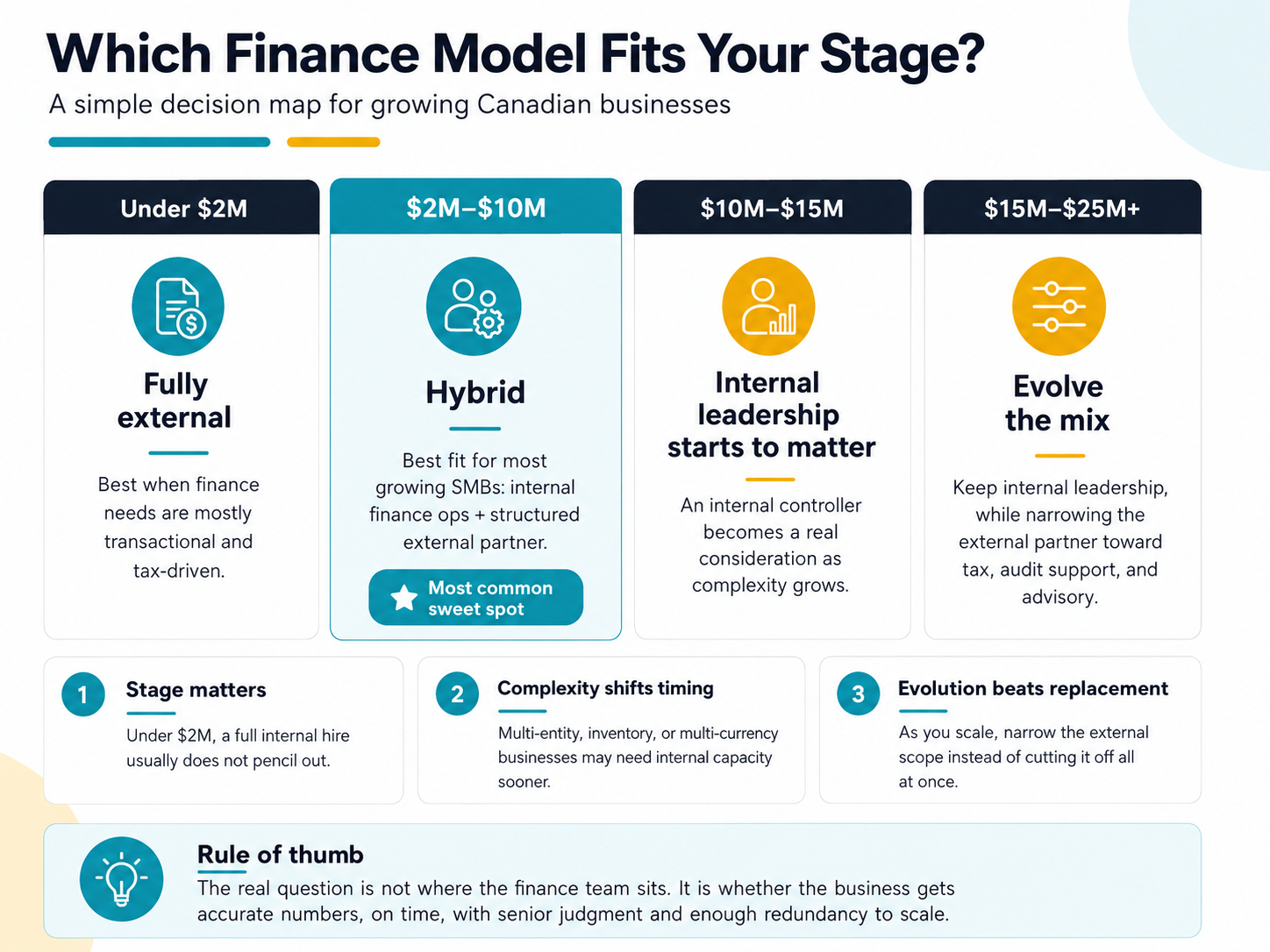

1. What stage are you at, honestly?

Under $2M, fully external is almost always right. The cost of an internal hire doesn't pencil out, and your finance needs are still mostly transactional and tax-driven.

Between $2M and $10M, hybrid is usually right. The split depends on your transaction volume, team size, and complexity.

Above $10M to $15M, internal leadership starts to matter more. A controller becomes a real consideration. The external relationship usually narrows but rarely ends.

2. How complex is your finance function?

Single-entity service business with predictable revenue? Less complexity, more leverage from external.

Multi-entity, multi-currency, inventory-heavy, or with significant intercompany transactions? More complexity, more pull toward dedicated internal capacity.

3. What's your growth trajectory?

Stable or slow-growth businesses can run leaner finance functions. High-growth businesses (planning to double or triple in 18-24 months) need finance infrastructure that scales ahead of the business, which almost always means external or hybrid because hiring can't keep pace.

4. How sophisticated does your decision-making need to be?

If you make most operational decisions on intuition and review financials quarterly, your finance function can be lighter. If you're making real-time pricing decisions, evaluating acquisitions, raising capital, or running a tight margin business where small variances matter, you need senior financial thinking on tap. That's almost always cheaper to get through fractional/external engagement than full-time hiring.

Mistakes we see both directions

A few patterns worth flagging, because they're costly and avoidable regardless of which model you pick.

Hiring an internal bookkeeper and expecting controller-level work. The job descriptions get blurred constantly. You hire someone at $65K and quietly expect them to perform like a $130K controller. They can't, and the books suffer.

Treating an external firm as a vendor instead of a partner. Throwing transactions over the wall, never sharing operational context, and then being surprised the reports don't reflect reality. The best outsourced relationships look like genuine partnerships, with regular operating reviews and open access to context.

Switching models too often. We've seen businesses go internal, then external, then back to internal in a span of three years. Every switch costs three to six months of disruption and meaningful cleanup expense. Pick a model, commit, and evolve it deliberately.

Underinvesting in systems regardless of model. Cloud accounting platform, payroll system, expense management, AR automation. The model matters less than the infrastructure underneath it. Sloppy systems make both internal and external setups fail.

Equating in-house with "more control." Control comes from documentation, process, and reporting cadence, not from physical proximity. A well-run external engagement with clear SLAs gives you more genuine control than a chaotic internal team you happen to see in the hallway.

The bottom line

The "internal vs. external accounting" debate is a false binary. The right answer for most growing Canadian businesses isn't one or the other. It's a deliberate construction of both, calibrated to your stage, complexity, and growth path.

What you're really choosing isn't a model. It's a finance function. The question isn't "where do these people sit?" It's "do I have accurate numbers, on time, every month, with senior judgment behind them, redundancy if someone leaves, and the ability to scale as the business grows?"

If your current setup delivers that, it doesn't matter much whether it's internal, external, or hybrid. If it doesn't, the gap is the real problem, not the org chart.

Key takeaways

- The real question isn't internal vs. external. It's which functions belong where, and how they connect.

- Cost favours external at lower complexity. Capability and reliability matter more once a business is established.

- External wins on systems, redundancy, and breadth of expertise. Internal wins on embedded context and immediate availability.

- Most $2M to $10M Canadian businesses are best served by a hybrid: a junior internal finance ops role plus a structured external partner.

- Each model breaks in predictable ways. Recognize the signs early and adjust before the cracks compound.

- The decision evolves with the business. Pick a model that fits today and plan for how it changes as you scale.

Frequently asked questions

Q: At what revenue level should I hire an internal accounting/finance team?

There's no universal answer, but the rough pattern in Canadian SMBs is: under $2M, almost never. $2M to $10M, hybrid usually beats a dedicated hire. Above $10M with operational complexity, an internal controller starts to make sense. The real trigger isn't revenue, it's transaction volume, complexity, and whether your CEO is doing finance work.

Q: Is an external accounting/finance team less secure than in-house?

Generally no. Reputable Canadian firms operate under professional confidentiality standards with documented access controls. The risk profile is often lower than relying on a single in-house employee with full access to your books. Where confidentiality concerns are real, structure the engagement accordingly with NDAs, restricted access, and clear data handling protocols.

Q: Can I have both an in-house bookkeeper and an external firm?

Yes, and this is the most common setup we see at scale. The internal person handles day-to-day operations and acts as the liaison. The external firm handles the close, reporting, compliance, and senior advisory. Done well, this is more cost-effective and more reliable than either model alone.

Q: What does a typical outsourced accounting engagement cost in Canada?

For a $2M to $10M business, monthly fees typically range from $2,500 to $8,000 depending on transaction volume, complexity, payroll size, and the level of advisory included. Tax-only relationships are cheaper. Full-service controllership and advisory engagements sit at the higher end.

Q: How do I know if my current external accountant is good enough?

A few quick tests: Are monthly reports delivered by day 10 or 15? Can they explain your numbers in plain language, not just hand you a P&L? Do they proactively flag issues, or only respond when asked? Are tax filings always on time, with no scramble? Have they helped you make a real decision in the past six months? If you're answering "no" to two or more, you've likely outgrown them.

Q: What's the cost of switching from internal to external (or vice versa)?

Variable, but always more than people expect. Plan for three to six months of dual cost and cleanup, plus potential delays in reporting during the transition. The cost is worth it when the current model is genuinely failing. It's not worth it for incremental gains. Switching is disruptive, so make the call deliberately.

Not sure whether your current finance setup is actually serving you? We help Canadian businesses structure finance functions that scale with them, whether that's fully external, hybrid, or transitioning toward an internal team. Book a free discovery session to see how we work with growing businesses.