Reconciliations have been categorized in business owners’ heads as administrative housekeeping. Something the back office does. Something that either happens or doesn't, and either way doesn't really affect how the business runs.

This is an expensive misunderstanding. Reconciliations are the single most reliable feedback loop a business has for catching errors, fraud, revenue leakage, and operational breakdowns before they compound. When it's done well and on time, it shapes every other financial decision in the company. When it's late, sloppy, or unsupervised, every report that flows out of your accounting system is a guess wearing a suit.

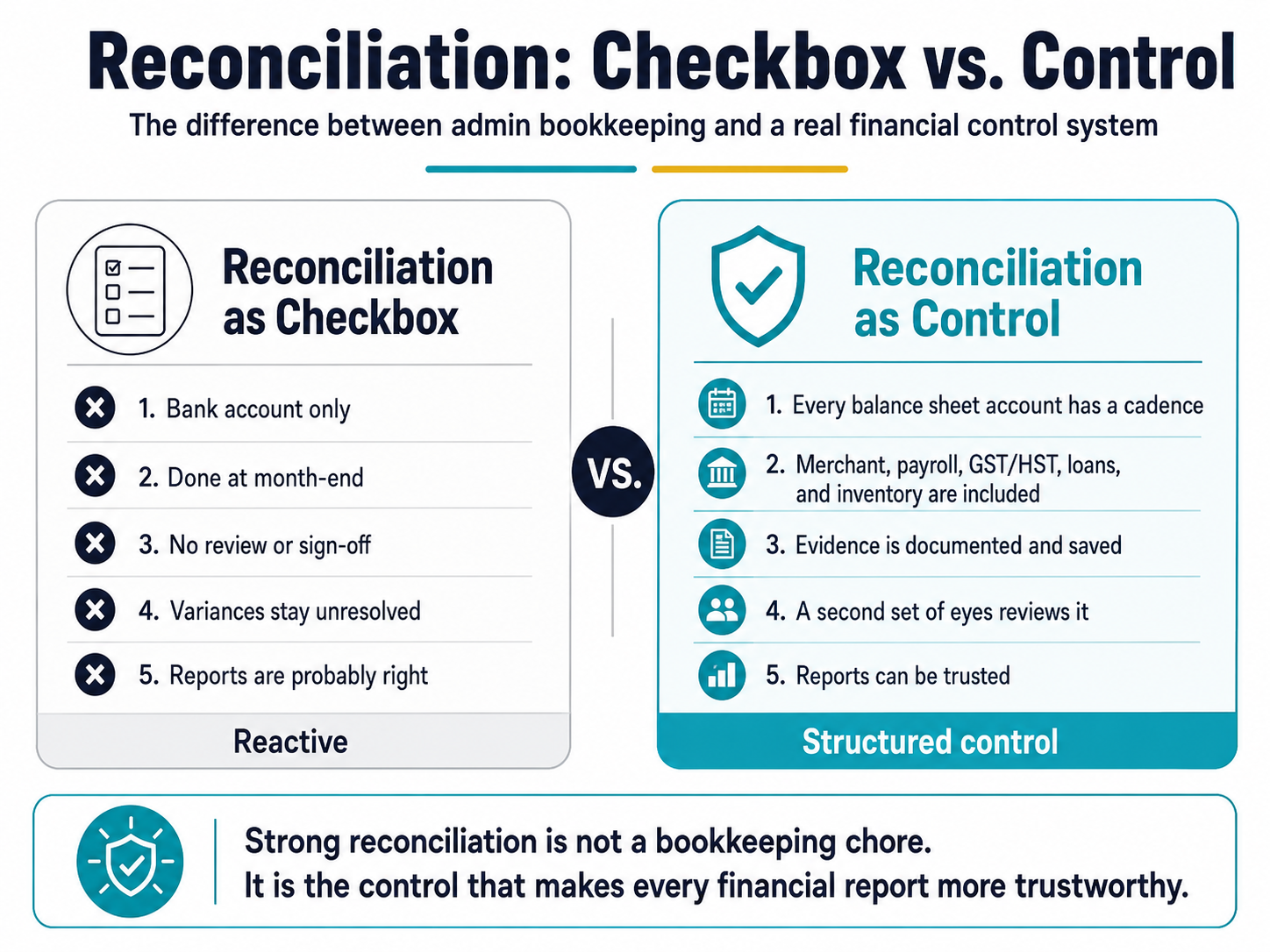

What a reconciliation is

In the textbook sense, a reconciliation is the process of matching transactions recorded in your accounting system against an independent source, usually a bank statement, credit card statement, or third-party report. If your books say you received $48,200 in deposits in October and your bank statement says the same, the account reconciles. If they don't match, you investigate the variance until they do.

That definition is technically correct and strategically useless.

The real function of reconciliations is verification. You are confirming, account by account, that what your business thinks happened actually happened, in the amounts it thinks, on the dates it thinks. Every other piece of financial reporting you produce, your profit and loss statement, your cash flow forecast, your tax filings, your investor updates, your loan covenants, depends on that verification being true.

Without it, you're not running on data - you're running on assumptions that look like data.

The accounts most growing businesses don't realize they should be reconciling

When founders think about reconciliations, they typically picture bank accounts. That's where most software-driven reconciliations live, and it's where bookkeepers spend most of their time. But in a $2M+ business, the accounts that quietly create the biggest problems are usually the ones nobody reconciles regularly:

- Credit card accounts, where employee spending, subscription creep, and miscategorized expenses pile up fast.

- Merchant processor accounts (Stripe, Square, Shopify Payments), where fees, refunds, chargebacks, and payout timing create constant variances.

- GST/HST control accounts, where collected and paid amounts need to tie out cleanly before a return is filed.

- Payroll clearing accounts, where remittances to CRA for CPP, EI, and income tax need to match what was actually withheld.

- Intercompany accounts, if you operate more than one entity.

- Loan and credit facility balances, where interest accruals and principal payments need to reconcile against the lender's statements.

- Inventory accounts, for product businesses, where what your books say you have should match what's actually on the shelf.

If your monthly close only reconciles your operating bank account, you have a partial reconciliation. Partial reconciliations produce partial truth.

The strategic cost of treating reconciliation as a checkbox

Here is where the framing shift matters. The cost of weak reconciliation is rarely visible in any single month. It compounds quietly across quarters, and then surfaces all at once at the moments that hurt most: a tax filing, a due diligence process, a CRA review, a cash crunch nobody saw coming.

Let me walk through what this actually looks like.

1. Decisions get made on numbers that aren't real yet

A SaaS company doing $4.2M ARR runs monthly P&L reviews. Revenue looks strong. Margins look fine. The founder approves a new hire in product, signs a longer-term office lease, and front-loads a Q4 marketing push.

What they don't see, because the books haven't been reconciled in seven weeks, is that the Stripe payout for September was double-counted (recorded both as a deposit and as a separate invoice payment), a $38,000 annual software contract was expensed entirely in one month instead of being amortized, and two large customer refunds were processed but never reflected in revenue.

The "real" revenue that month was about $61,000 lower than the report showed. Margins were three points worse. The hiring decision and the lease were both made on numbers that simply weren't accurate yet.

This is not a hypothetical. It is the single most common pattern we see in businesses between $2M and $10M. The numbers feel solid because they came out of accounting software. But unreconciled software output is not finalized data. It's a draft.

2. Revenue and expense leakage hide in plain sight

A clean reconciliation forces you to look at every transaction, every variance, every unexplained line. That process surfaces things that nobody would otherwise notice:

- A monthly subscription that was supposed to be cancelled in March but is still charging in October.

- A vendor that double-billed for three months running, where the first invoice was paid each month and the duplicate was filed away.

- A client whose recurring invoice was set up incorrectly and has been undercharging by 15% for the last year.

- A merchant processor pulling a higher fee rate than the contract specifies.

- Employee expense reports being reimbursed without supporting receipts.

For a business doing $4M in revenue, leakage in the 1–3% range is almost always present. Most owners are stunned when they find it, because the dollar amounts are not trivial: $40,000 to $120,000 a year in some combination of overpayments, missed billings, and stale subscriptions. That money was never visible because nobody was looking line by line. Reconciliation is the only process that forces line-by-line examination.

3. Fraud and process failures live in the gap

The vast majority of small business fraud is internal, low-sophistication, and entirely preventable. It's usually not the dramatic scenarios people imagine. It's a bookkeeper running personal expenses through the company card. It's a manager approving their own reimbursements. It's a vendor that doesn't actually exist, with payments routing to a personal account.

The single most effective control against this kind of fraud is segregation of duties combined with regular, independent reconciliation. Not because reconciliation catches every scheme directly, but because anyone who knows the books are being reviewed monthly behaves differently than someone who knows they aren't.

When reconciliation is late, infrequent, or done by the same person who records the transactions, that control disappears. The risk doesn't feel real until the day it is, and by then, the losses are often into six figures.

4. CRA exposure quietly accumulates

In Canada, the CRA expects your records to support every number on your tax filings: corporate tax, GST/HST, payroll remittances, T4s, T4As. If you're audited or reassessed, the CRA isn't looking at your software dashboard. They're looking at whether your reported numbers tie to source documents and reconciled accounts.

Common issues that surface in reviews:

- GST/HST collected on revenue that wasn't actually reconciled to deposits, leading to over-remittance.

- Input Tax Credits claimed on expenses that don't have supporting reconciliation or receipts, leading to denied claims and interest.

- Payroll remittances that don't tie out to what was actually withheld, triggering reassessment and penalties.

- Revenue figures on the T2 that don't reconcile to bank deposits, raising questions about completeness.

None of these are exotic. All of them flow directly from reconciliation gaps. And the cost isn't just the tax adjustment. It's the time, the professional fees, and the years of additional scrutiny that follow a reassessment.

5. You lose the ability to close the month on time

The single best operational indicator of finance maturity is how many business days it takes a company to close its books each month. Best-in-class operators close in 5 to 7 business days. Healthy growing businesses close in 10 to 15. Businesses with reconciliation issues often can't close at all in any meaningful sense. They produce a P&L that they know is approximate, label it final, and move on.

A delayed or unreliable monthly close has cascading effects: investor reports go out late or wrong, board meetings happen without current numbers, cash flow forecasts are built on stale data, and tax planning becomes reactive instead of strategic. Reconciliation is the bottleneck. Fix it, and the close tightens. Leave it broken, and every downstream process inherits the dysfunction.

What a "good" reconciliation looks like

In a healthy finance operation, reconciliation isn't a single task at month-end. It's a structured rhythm with clear ownership and clear evidence.

The rhythm

For most $2M–$10M businesses, the practical cadence looks like this:

Operating bank accounts and credit cards should be reconciled at least monthly, ideally with a mid-month interim check. Merchant processor accounts (Stripe, Shopify, Square) need to be reconciled monthly without exception, because payout timing creates predictable variances that compound if ignored. GST/HST control accounts should be reconciled in the same cycle as your filing frequency: monthly if you file monthly, quarterly if you file quarterly. Payroll clearing should be reconciled every pay cycle. Loan and credit facility balances should be reconciled monthly against lender statements. Intercompany balances should be reviewed and confirmed monthly.

Inventory, for product businesses, should be physically counted at least quarterly with reconciliation back to the system count. Service businesses with significant work-in-progress or unbilled revenue should reconcile their WIP accounts monthly.

The point isn't the calendar. The point is that every account on your balance sheet has a documented schedule for verification, and someone owns it.

The evidence

A reconciliation isn't done when the numbers match. It's done when you have documented evidence of the match. That means:

- A reconciliation report from your accounting software, showing the cleared balance, the unreconciled items, and the date.

- Supporting documentation for any reconciling items (deposits in transit, outstanding checks, timing differences).

- A review signature or sign-off from someone other than the person who performed the reconciliation.

- A clean audit trail that another professional could pick up and follow.

If your bookkeeper "reconciles" your accounts but can't produce these artifacts on demand, your reconciliation isn't an actual control. It's a name on a task list.

The separation

This is the part most growing businesses get wrong. The person who records transactions should not be the only person reviewing reconciliations. This isn't about distrust. It's about basic financial controls. When the same person enters the data and verifies the data, errors and irregularities can persist for years without detection. Small businesses solve this with a second set of eyes: a fractional controller, an external accountant, or at minimum the owner doing a meaningful monthly review.

The signals your reconciliation is broken

Most founders don't know whether their reconciliation process is healthy because they've never had a baseline to compare it to. Here are the patterns that almost always indicate something is wrong, even if nobody has flagged it yet.

You can't answer "when were the books last reconciled?" within 30 seconds.

If the answer requires a Slack message to your bookkeeper, the process isn't visible enough to be working.

Your monthly P&L changes after it's been "finalized."

A correctly closed month doesn't move. If September's revenue number is different in November than it was in October, something upstream is being reworked, and that something is usually reconciliation.

You discover stale subscriptions, duplicate charges, or billing errors more than a few times a year.

Healthy reconciliation surfaces these almost immediately. If you're finding them at random, it means nobody is looking systematically.

Your GST/HST filings require last-minute scrambles.

A filing should be a five-minute confirmation of a balance that's already been reconciled, not a frantic reconstruction.

Your year-end is a multi-week project for your accountant.

A clean monthly close means year-end is mostly already done. If your accountant is doing material adjustments in March or April, those adjustments are almost always reconciliation cleanup.

Your bookkeeper's reports include unexplained variances or "to be reviewed" line items that persist month over month.

Open items that don't close are a sign that reconciliation is happening on the surface but not being driven to completion.

Any one of these in isolation is worth a conversation. Two or more, and the process needs structural attention, not just a reminder to be more careful next month.

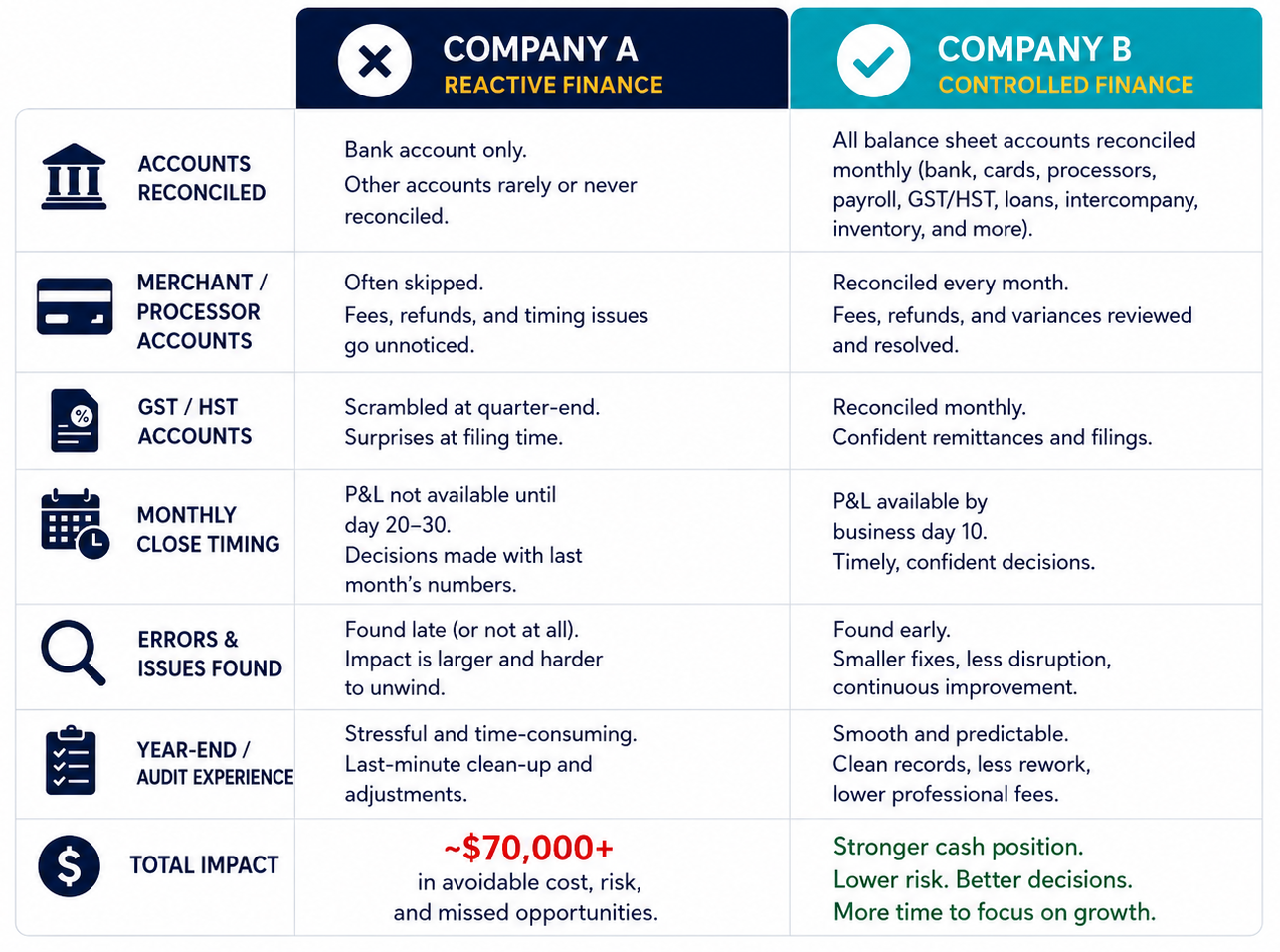

What this looks like in practice: a tale of two businesses

Two e-commerce companies, both doing roughly $6M in annual revenue, both selling primarily through Shopify with some Amazon and wholesale revenue mixed in.

Company A has a bookkeeper who reconciles the operating bank account monthly. Stripe and Shopify Payments are "tracked" but not formally reconciled because the bookkeeper finds them confusing. The GST/HST account is balanced once a quarter, the night before the filing is due. There's no documented close process. The owner gets a P&L sometime between the 20th and the 30th of the following month, depending on workload.

In the last 18 months, Company A has discovered:

- A duplicate inventory charge from a supplier that ran for four months. About $14,000.

- A Shopify Payments fee rate that was higher than the contract specified, caught only when the owner happened to ask. Recovery: $9,200.

- A misclassified $42,000 capital purchase that was expensed in full, resulting in an inaccurate tax filing that had to be amended.

- A six-month payroll remittance variance that the CRA flagged, triggering a review and penalties of roughly $4,800.

Total visible cost: about $70,000, plus the time and stress of cleanup. The invisible cost (months of decisions made on shaky numbers, delayed reports, missed tax planning opportunities) is harder to quantify but almost certainly larger.

Company B uses the same software and runs at the same revenue level, but has a defined month-end close process. Every balance sheet account is reconciled monthly, including merchant processors, GST/HST, payroll clearing, and inventory. The reconciliations are reviewed by an external controller before the books are closed. Variances are investigated and resolved before the P&L is issued, typically by business day 10.

Over the same 18 months, Company B caught a vendor double-billing in the first month it happened (recovered immediately), identified two pricing errors on recurring customer invoices that were quietly costing the business about $30,000 a year, and walked into their CRA filing season with zero adjustments needed. Their year-end took the accountant four days to finalize. Their last investor update went out on the 12th of the month, with reconciled numbers.

Same revenue. Same software. Completely different operational reality. The difference isn't tools. It's how reconciliation is treated.

Where most growing businesses go wrong

A few patterns come up consistently when reconciliation breaks down in scaling businesses.

The first is over-reliance on bank feed automation. Modern accounting software pulls bank transactions in automatically and matches them to recorded entries based on rules. This is useful, but it is not a reconciliation. It's a transaction import. True reconciliations are the act of comparing the final reconciled balance against the bank statement and explaining every difference. Automation handles the easy 80% and leaves the messy 20% (the part that matters) for a human to resolve. Many businesses skip the messy 20%.

The second is unclear ownership. The owner assumes the bookkeeper handles it. The bookkeeper assumes the accountant catches anything important at year-end. The accountant assumes the bookkeeper has cleaned things up before the year-end package arrives. Nobody owns the reconciliation review, and so it doesn't really happen with rigor.

The third is treating it as the last priority instead of the first. When the bookkeeper's workload gets heavy, reconciliations are what get deferred because it doesn't have an external deadline the way payroll or invoicing does. The deferred reconciliation then makes every subsequent month harder, because errors compound.

The fourth, and arguably the most expensive, is assuming software equals accuracy. Cloud accounting tools are powerful, but they categorize and match based on rules you (or a previous bookkeeper) set up. They reflect those rules faithfully, including when those rules are wrong. Software without human reconciliation produces confidently incorrect books at scale.

This is where having a structured monthly close process, with reconciliation as a deliberate, reviewed step rather than an assumed background task, makes the operational difference. Most $2M–$10M businesses don't need a full-time controller to get this right. They do need someone, internal or fractional, whose job explicitly includes owning the reconciliation review.

Final Thoughts

Reconciliation gets dismissed as administrative work because it doesn't generate revenue, doesn't impress investors, and doesn't make for good LinkedIn content. It just quietly determines whether the numbers your business runs on are real.

A growing business with weak reconciliation is making real decisions on approximate data. Sometimes it works out. Often it doesn't. And the failures, when they come, tend to come all at once: a botched tax filing, a due diligence disaster, a fraud discovery, a cash crunch that wasn't supposed to be possible.

A growing business with strong reconciliation has a feedback mechanism that catches errors before they compound, surfaces money that would otherwise leak away, builds the foundation for a clean monthly close, and produces reports that founders and boards can actually trust. The cost is modest. The return is structural.

If reconciliation in your business is currently a checkbox, the most useful thing you can do is stop treating it that way. Define the cadence. Assign the ownership. Require the evidence. Build the second set of eyes into the process. Done well, it stops being the boring part of finance and becomes one of the most valuable controls you have.

Key takeaways

- Reconciliation isn't a bookkeeping chore. It's a verification process that determines whether every other financial report you produce can be trusted.

- Most growing businesses only reconcile their operating bank account. The accounts that quietly create problems (merchant processors, GST/HST, payroll clearing, credit cards) are often the ones nobody touches monthly.

- Weak reconciliation produces decisions made on approximate data, hidden revenue and expense leakage, fraud risk, CRA exposure, and an inability to close the month on time.

- Good reconciliation has three components: a defined rhythm, documented evidence, and separation between the person recording transactions and the person reviewing the reconciliation.

- Software automates the easy 80%. The remaining 20% is where mistakes live, and skipping it is the most common reason reconciliation fails at scale.

- Most $2M–$10M businesses don't need a full-time controller. They do need someone whose job explicitly includes owning the reconciliation review.

Frequently asked questions

Q: How often should reconciliation actually be done?

At minimum, monthly for all balance sheet accounts. Operating bank accounts and merchant processors benefit from a mid-month interim check. Payroll clearing should reconcile every pay cycle. The right cadence is whatever produces a clean, closed set of books within 10 to 15 business days of month-end.

Q: Isn't this what our accounting software does automatically?

No. Software imports transactions and matches them against rules. True reconciliation compares the final reconciled balance to the source statement and explains every variance. Automation handles the routine matches; reconciliation is the act of resolving everything that doesn't auto-match and confirming the final position.

Q: Our bookkeeper handles reconciliation. Should we be doing anything else?

Two things. First, ask to see the reconciliation reports and supporting documentation, not just the P&L. Second, make sure someone other than the bookkeeper is reviewing those reconciliations before the books are closed. That second set of eyes is the actual control.

Q: What's the difference between reconciliation and a month-end close?

Reconciliation is a component of the close. A complete month-end close also includes journal entries, accruals, depreciation, intercompany activity, and review of the P&L and balance sheet. But reconciliation is the foundation: without it, the rest of the close is unreliable.

Q: How do I know if our reconciliation process is working?

Three quick tests. Can you produce reconciliation reports for every balance sheet account from last month within an hour? Does your P&L from three months ago still show the same numbers today? Has your accountant told you year-end is straightforward? If yes to all three, your process is probably healthy. If no to any, it's worth a deeper look.

Q: We're a $3M business. Do we really need this level of rigor?

Yes, and arguably more than larger businesses do. At $3M, you don't have the internal finance bench to absorb errors quietly. A single material reconciliation failure can directly hit owner take-home, tax position, or hiring decisions. The discipline costs less than the alternative.

If reconciliation has quietly become a question mark in your business, or if you're not entirely sure how rigorous your current process is, we'd be happy to take a look. We provide controllership and monthly accounting services for businesses that have outgrown a simple bookkeeping setup and need a finance function that actually closes the loop. Book a complimentary call to learn more about our controllership services.