The conversation almost always starts the same way. A founder calls their accountant in May, eighteen months after taking money out of their corporation, and learns that the $180,000 they pulled "as a shareholder loan" is now being added to their personal income. The tax bill is real, the interest is compounding, and the explanations for this result are difficult to understand.

This is known as the dreaded “subsection 15(2) trap”. It is one of the more expensive surprises in Canadian small business tax, and the danger is how quietly it happens. In practice, there is very little warning from the CRA before they invoke subsection 15(2) of the Income Tax Act (the “Act”) and reassess with taxes, interest, and penalties. The singular cause is often a balance on the shareholder loan account that was not cleared in time.

What makes this trap especially dangerous is that it is often a bookkeeping issue first and a tax issue second. The exposure quietly builds inside the general ledger, before anyone is thinking about year-end. By the time the accountant sees it, the window to fix it cleanly has often already closed.

This guide walks through how the trap actually works, why the one-year rule trips up even careful owners, the bookkeeping mechanics that create exposure without anyone noticing, the legislative exceptions that provide some planning room, and what a clean draw structure should look like. However, this guide does not constitute specific tax advice, and readers are encouraged to speak to their tax accountant to properly identify and proactively resolve any shareholder loan issues before a reassessment arrives.

What Subsection 15(2) Does

Section 15 of the Act is the provision that polices how shareholders extract value from their corporations. Subsection 15(2) deals specifically with loans and indebtedness, and the rule it sets is clear and straightforward.

If a shareholder or someone connected to a shareholder becomes indebted to the corporation, the full principal amount of that debt is included in the shareholder's personal income in the year the loan was made. The entire balance flows through to the shareholder’s personal tax return as ordinary income, taxable at his or her marginal rate.

To illustrate, a founder in Ontario at the top marginal bracket who takes a $200,000 shareholder loan and gets caught by s.15(2) is looking at roughly $107,000 in personal tax on money they may have already spent.

This provision is legislatively designed to be broad. It exists because shareholders could otherwise strip cash out of their corporations indefinitely, calling it a "loan" and never paying the personal tax that salary or dividends would trigger. Subsection 15(2) closes that door.

But the Act also recognizes that not every shareholder loan is tax avoidance. There are legitimate reasons for owners to borrow from their corporations, and the legislation provides two main escape hatches: the one-year repayment exception in subsection 15(2.6), and the specific-purpose exceptions in subsection 15(2.4). Understanding both is what separates owners who use shareholder loans as a planning tool from owners who get blindsided by them.

The One-Year Rule

The subsection 15(2.6) exception is the one most business owners have heard of, but the technical nuances make it tricky to apply correctly.

A loan to a shareholder will not be included in income under subsection 15(2) if it is repaid within one year after the end of the taxation year of the corporation in which the loan was made - provided the repayment is not part of a series of loans and repayments.

There are three components that business owners can get wrong.

Component one: The clock starts at year-end, not at the loan date

The clock does not start ticking on the day you take the loan. Rather, it starts at the end of your corporation's fiscal year.

Consider a corporation with a December 31 year-end. A shareholder loan taken on January 15, 2025 must be repaid by December 31, 2026 to qualify for the exception. In this example, that is almost two full years. However, the same loan taken on December 20, 2025 must also be repaid by December 31, 2026 - barely twelve months later.

The strategic implication is significant. Loans taken early in the corporation’s fiscal year can give business owners almost 24 months of breathing room. On the other hand, loans taken late in the fiscal year provide only just over 12 months. Business owners who do not think about timing routinely take year-end draws that have almost no recovery window built in.

Component two: "Repaid" means actually repaid

The repayment has to be genuine. A journal entry reclassifying the loan as a dividend at year-end can potentially work, but it must be supported by a proper directors' resolution declaring the dividend, the corresponding T5 filing, and the personal tax that follows.

A book entry alone - moving the balance from "Shareholder Loan" to "Shareholder Loan - Bob" and back - does not extinguish the debt. The CRA is alert to circular movements, and so is the legislation, which brings us to the third component.

Component three: The "series of loans and repayments" disqualification

This is where most planning goes off the rails. Even if you repay the loan within the window, the s.15(2.6) exception does not apply if the repayment is part of a series of loans and repayments.

What does that mean in practice? It means you cannot repay the loan on December 30 and borrow it back on January 5. The CRA will look at the substance. If the pattern shows that the business owner is recycling the same money to avoid the income inclusion, the exception is denied - sometimes years after the fact, during a reassessment.

This is not a hypothetical risk; it is one of the most common ways the trap actually closes on otherwise compliant owners. The intent of the provision is that the loan be genuinely repaid, rather than part of an ongoing arrangement to keep funds out of the corporation indefinitely.

An example with real dates

Assume a corporation with a fiscal year ending June 30.

If the shareholder repays $200,000 on June 25, 2026, the July 2024 and March 2025 loans are cleared on time. The August 2025 loan remains outstanding, with its own deadline a year later. If he or she then borrows $200,000 again on July 5, 2026, the CRA will consider that pattern as “a series of loans and repayments” and disallow the exception for the earlier loans, resulting in the CRA going back and reassessing these years.

This example illustrates that the dates and the pattern both matter and must be defensible.

.png)

Deemed Interest

There is a second, separate tax issue that operates regardless of whether subsection 15(2.6) saves the business owner from an income inclusion. Even a perfectly compliant shareholder loan creates a taxable benefit if it is interest-free or below-market.

Under subsection 80.4(2), a shareholder who receives a low-interest or interest-free loan from their corporation is deemed to have received a taxable benefit equal to the difference between interest at the CRA's prescribed rate and the interest actually paid. The rate used to calculate taxable benefits for employees and shareholders from interest-free and low-interest loans is currently 3% for Q2 2026.

In practice, this means a $200,000 interest-free shareholder loan outstanding for a full year produces a deemed benefit of $6,000, which is added to the shareholder's personal income.

This is a relatively smaller tax issue than the subsection 15(2) inclusion, but it is separate and additive. Owners sometimes assume that because the loan is otherwise compliant, no tax consequences attach to it - which is not true.

Fortunately, there can be a workaround. If the shareholder pays interest to the corporation at the prescribed rate (or higher) and pays it within 30 days of year-end, the deemed benefit is generally eliminated. The corporation then includes that interest in its income. The net effect, depending on the structure, can be cleaner than absorbing the personal benefit year after year.

Incidentally, this is also the rate the CRA uses for the section 80.4 calculation. Different prescribed rates apply to overdue tax balances (7% as of Q2 2026), which is what you would pay if a subsection 15(2) inclusion is reassessed years after the fact. The combination - back tax on the principal at marginal rates, plus 7% interest compounded daily - is what turns a $200,000 oversight into a potential $250,000+ liability by the time it surfaces.

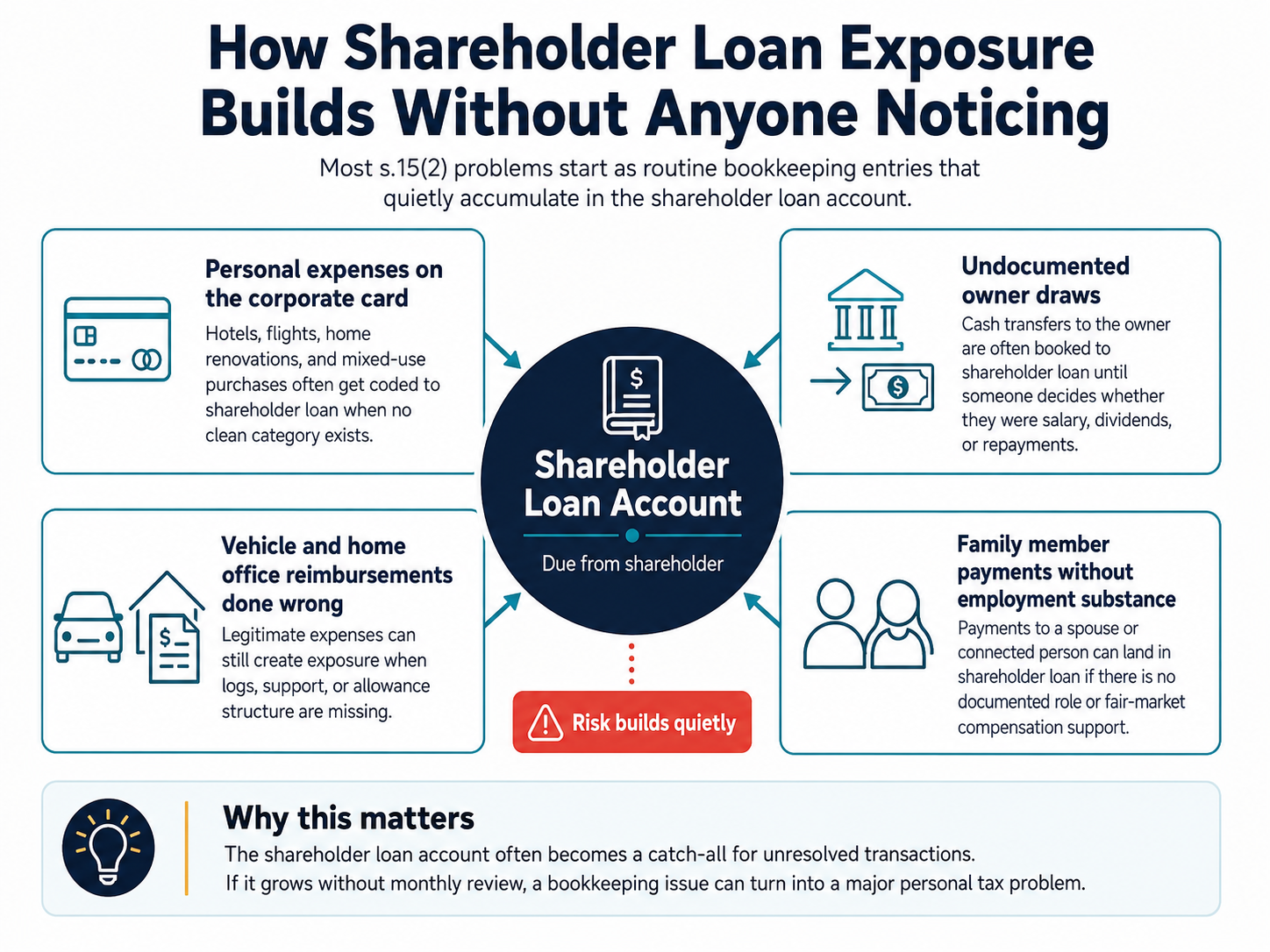

The Bookkeeping Mechanics that Hide the Tax Exposure

This is the section most tax-firm content skips, and it is the one that matters most operationally. The subsection 15(2) problem is almost always created in the general ledger - specifically, by routine entries that no one flags as risky at that particular time. However, by the time the accountant prepares year-end financials, the exposure is already on the balance sheet.

In our experience, here are the four entries that most often quietly build a shareholder loan position.

Personal expenses run through the corporate account

This item is the most common pattern. A founder uses the corporate Visa for a personal hotel, a family flight, a home renovation deposit, or a Costco run that may be 70% personal. The bookkeeper, unsure how to categorize it and uncomfortable confronting the owner, codes it to "Shareholder Loan – Due From Shareholder."

Over a year, this kind of drift can easily add $30,000 to $80,000 to the shareholder loan balance without anyone making a deliberate decision:

- The owner is unaware that the account is growing.

- The bookkeeper assumes the accountant will sort it out at year-end.

- The accountant sees the balance for the first time in March of the following year, when the window to act is rapidly closing.

Undocumented owner draws

This item is another common pattern: The business owner needs cash and transfers (say) $15,000 from the corporate account to their personal account, intending to "figure it out later" whether it is a salary draw, a dividend, or a loan repayment. In the absence of any documentation, the bookkeeper books it to the shareholder loan account by default.

Repeated over a year, this creates a balance that the owner experiences as their own money, but the Act treats as an outstanding loan subject to subsection 15(2).

Vehicle and home office reimbursements done wrong

If a corporation reimburses an owner for vehicle expenses or home office costs without a proper allowance structure or supporting log, the reimbursement may be recharacterized. Sometimes it sits in the shareholder loan account as a workaround for not having the documentation to support a legitimate expense deduction.

This one is particularly tricky because the underlying transaction is often legitimate: The expense is real, and the owner did drive the vehicle for business. However, without the documentation and structure to support it as a corporate expense or a properly designed allowance, it ends up parked in the shareholder loan account, creating exposure.

Family member payments without employment substance

A spouse is paid through the corporation. However, the spouse does not actually perform the services, or the payments are not at fair market value, or there is no documentation supporting their role. The bookkeeper, again uncomfortable categorizing it as wages without substance, posts it to the shareholder loan account as a related-party payment.

Furthermore, the loan is not even to the registered shareholder - it is to a person connected to the shareholder, which subsection 15(2) explicitly captures. The owner often does not realize the family member's draws are landing on their personal tax exposure.

The pattern

In every case, the shareholder loan account functions as a catch-all for transactions the books cannot otherwise resolve. It is the financial equivalent of a desk drawer where uncomfortable items get filed. And because most monthly bookkeeping reviews focus on profit and loss rather than balance sheet drift, the account grows without scrutiny.

A real controllership function catches this on the monthly close. A bookkeeper working in isolation often does not.

The Subsection 15(2.4) Exceptions

As noted above, the Act recognizes that some shareholder loans serve legitimate purposes beyond simply extracting cash. In this regard, subsection 15(2.4) carves out specific exceptions where loans to shareholders who are also employees can avoid the subsection 15(2) income inclusion entirely, subject to strict conditions. Generally, the subsection 15(2.4) exceptions apply broadly to employees. However, for specified employees, the CRA scrutinizes whether the loan was made "because of" their employment or "because of" their shareholding; only the former qualifies in these cases.

Two requirements apply to these exceptions and must be met before any of the specific tests apply.

- The bona fide repayment requirement. At the time the loan is made, bona fide arrangements must be in place for repayment within a reasonable time. This means ordinary documented loan terms (e.g. interest rate, repayment schedule, security if applicable) must be in place. It cannot be a handshake or inferred agreement; rather, the repayment plan must exist on paper and be reasonable in commercial terms.

- The employee-shareholder test. The borrower must be an employee of the corporation (or the corporation's affiliated corporation). Holding shares alone is not enough. There must be an actual employment relationship with employment income flowing through it. This trips up owners who have not run themselves on payroll.

With those two preconditions in place, four specific-purpose exceptions become available.

Loans to acquire a dwelling for the employee's own use

A corporation can lend an employee-shareholder funds to acquire (or refinance debt on) a home for their own habitation. The exception covers the actual residence - not a vacation property, not a rental, not a property held in a separate corporation. Documentation must support that the property is for the borrower's own use.

This is a potentially meaningful planning lever for business owners who would otherwise need to draw substantial after-tax dollars to put toward a home purchase. The corporation can lend the funds at the prescribed rate (the section 80.4 benefit still applies if the rate is below the prescribed rate), and the loan can be repaid over a commercially reasonable period.

Loans to acquire newly issued shares of the corporation

If an employee-shareholder needs to fund the purchase of newly issued shares of the corporation (or an affiliated corporation), the loan to do so can qualify for the exception. This is most often used in various structuring scenarios: Bringing in key employees as minority shareholders, share reorganizations, or estate freezes where the next generation acquires shares - areas that our special tax team can assist with.

The condition that the shares be newly issued is important. Loans to fund the purchase of existing shares from another shareholder do not qualify.

Loans to acquire a motor vehicle used in the course of employment

A corporation can lend an employee-shareholder funds to acquire a vehicle used in the performance of their employment duties. The deductibility tests for employment use have to be satisfied. The vehicle has to actually be used for the business in a meaningful way - not nominally.

In practice, this is the narrowest of the four exceptions and the one most likely to be challenged on facts. The cleaner approach for most businesses is to have the corporation own or lease the vehicle directly and structure the personal-use benefit through standard mechanisms.

Loans in the ordinary course of the corporation's money-lending business

If the corporation is in the business of lending money, and the loan to the shareholder is made on the same commercial terms as loans to arm's-length parties, it falls outside subsection 15(2). This exception applies only to corporations whose actual business is money-lending - finance companies, certain holding structures, and not to ordinary operating businesses that happen to make a loan.

The general principle behind the exceptions

What unifies all four is that they cover situations where the corporation is acting in a quasi-commercial capacity - lending for purposes that have substance independent of tax extraction. The Act is willing to permit the loans, but only with documentation, employment substance, bona fide repayment terms, and use restrictions in place.

For owners in the $2M to $10M range, the housing and share acquisition exceptions are the most commonly useful. Both require deliberate structuring before the loan is made, not after. Retroactive characterization rarely survives scrutiny.

Designing a Draw Structure that Minimizes Tax Exposure

The most effective protection against subsection 15(2) is not a clever year-end maneuver - it's a draw structure that does not accumulate exposure in the first place. Here is what that looks like in practice for a typical owner-operated business.

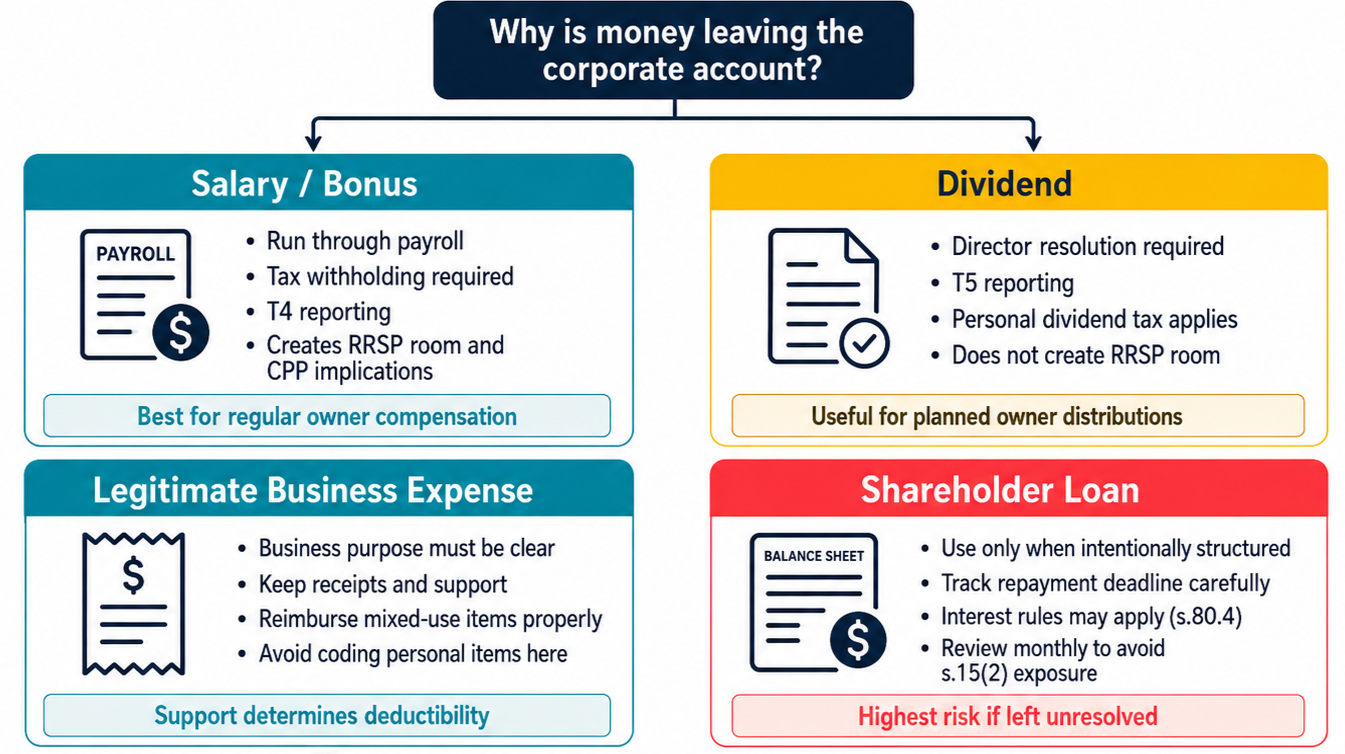

Decide your compensation mix annually, in advance

Salary, bonus, dividends, and shareholder loans are not interchangeable. They have different tax characteristics, different cash timing, and different downstream implications for RRSP room, CPP entitlement, and corporate retained earnings.

The decision of how you will pay yourself should be made before the fiscal year starts, in conversation with your accountant, and documented. Most exposure builds when this decision is made by default - by what is in the corporate account on any given Tuesday, rather than by design.

Run a regular, scheduled salary or dividend

If you draw money out of the corporation, the cleanest mechanism is a predictable, documented monthly amount via payroll (for salary) or a documented dividend resolution (for dividends). When the regular draw covers your living expenses, the shareholder loan account doesn't need to absorb ad-hoc transfers.

The pattern to avoid: irregular transfers from the corporate account whenever personal cash is tight, with no payroll or dividend documentation supporting them. That is the highway to a six-figure shareholder loan balance.

Use a separate personal credit card

The single most effective bookkeeping control for subsection 15(2) exposure is the boring one: stop using the corporate card for personal purchases. Even legitimate gray-area purchases (the dinner that's half personal, the trip with mixed business) belong on a personal card with the business portion reimbursed via expense report.

Mixed transactions on the corporate card are the most common source of bookkeeper-driven shareholder loan accumulation. They also flag clearly in any audit.

Reconcile the shareholder loan account monthly, not just at year-end

The shareholder loan account should be reviewed on every monthly close, with every entry justified and documented. If the balance is moving, the owner should know why. If transactions are being coded there because no other category fits, that's a signal - not a satisfactory resolution.

A well-run finance function treats this account as one of the most sensitive lines on the balance sheet. Most businesses treat it as the least.

Plan dividend declarations to clear balances before year-end deadlines

If a shareholder loan balance is sitting on the books and approaching its subsection 15(2.6) deadline, the most common clean exit is to declare a dividend before year-end equal to the balance and apply it against the loan. This converts the loan into a dividend, triggers the dividend tax (at integrated rates that are usually much friendlier than subsection 15(2) inclusion would be), and clears the exposure.

The mechanics matter: directors' resolution, T5 filing, dividend tax credit on the personal return. Done right, it's a planning tool. Done verbally and recorded as a journal entry only, it doesn't hold up.

When the Trap has Already Closed

If you realize your shareholder loan balance is past its subsection 15(2.6) window (or close to it), there are still options - but they narrow quickly.

Within the window: clear the balance through a declared dividend, a payroll-based bonus, or actual cash repayment from personal funds. The cleanest of the three depends on your personal tax position, the corporation's small business deduction room, and cash availability.

Just past the window: voluntary disclosure to the CRA may be available, depending on the facts. The Voluntary Disclosures Program can reduce penalties and partial interest if the disclosure is voluntary, complete, involves a penalty, and is more than one year overdue. This is a path that needs to be walked with professional support.

Years past the window with no disclosure: generally speaking, this is the worst position to be in. If the CRA identifies the exposure in audit, you are looking at the income inclusion in the original year, interest at the prescribed overdue rate (currently 7%, compounding daily), and potentially gross negligence penalties. The combined cost frequently exceeds the original loan amount.

The takeaway: Act early. The cost of fixing a subsection 15(2) exposure when you spot it is almost always a fraction of the cost when the CRA spots it.

Final Thoughts

Subsection 15(2) is one of those provisions of the Act that rewards owners who understand it and punishes owners who do not. The mechanics can be nuanced, but are not fundamentally difficult to apply with due care. The challenge is that exposure typically accumulates inside the general ledger before it surfaces as a tax problem, and most businesses do not have a financial function that monitors the shareholder loan account closely enough to catch the drift.

There are three things that business owners can do to mitigate risk.

- Treating the shareholder loan account as a sensitive line on the balance sheet, reviewed monthly, with every entry justified.

- Designing a draw structure in advance - knowing how money will leave the corporation, in what form, and on what schedule - so that the loan account is not quietly absorbing ad-hoc transactions.

- Bringing tax planning into the conversation early enough that the subsection 15(2.4) exceptions, the dividend mechanics, and the one-year window can all be used as planning tools rather than salvage operations.

This is the kind of work a real finance function does - maintaining disciplined, monthly visibility on the shareholder loan account (which causes the most damage when left alone).

Five Key Takeaways

- The subsection 15(2) inclusion is the principal, not the interest. A shareholder loan that misses its repayment window is added to personal income at marginal rates.

- "Series of loans and repayments" is the most overlooked disqualifier. Repaying and re-borrowing the same balance does not preserve the subsection 15(2.6) exception.

- The section 80.4 deemed interest benefit applies separately. A compliant shareholder loan still produces a taxable benefit if it is interest-free, at 3% of the balance per year (Q2 2026 prescribed rate).

- Most exposure is created by routine bookkeeping. Personal expenses on the corporate card, undocumented draws, vehicle reimbursements without structure, and family member payments are the most common silent accumulators.

- Design the draw structure in advance. The most reliable protection is a predictable compensation mix decided annually and supported by documentation, not year-end maneuvers.

Frequently Asked Questions

Q: I took $80,000 out of my corporation last year, and it's sitting in my shareholder loan account. Am I in trouble?

Not necessarily. It depends on your corporation's fiscal year-end, when the loan was taken, and what your repayment plan looks like. If you're within the subsection 15(2.6) window - one year after the end of the fiscal year in which the loan was made - you still have options to clear the balance cleanly through a declared dividend, payroll, or cash repayment. The conversation to have with your accountant is about timing and method, not panic.

Q: Can I just repay the loan and borrow it back the next day?

No. This is the "series of loans and repayments" scenario, and it is specifically excluded from the subsection 15(2.6) exception. The CRA can reassess years after the fact if a pattern of repayment and re-borrowing emerges. The repayment has to be genuine.

Q: What's the difference between a shareholder loan and a director's loan?

For Canadian tax purposes, both are captured by subsection 15(2) if the borrower is a shareholder or connected to a shareholder. The terminology used in your bookkeeping software doesn't change the tax treatment. What matters is the actual relationship between the borrower and the corporation.

Q: Does subsection 15(2) apply if I lend money to my corporation, rather than the other way around?

No. Section 15(2) deals only with loans from the corporation to the shareholder. Loans from the shareholder to the corporation (often labeled "Due to Shareholder" on the balance sheet) raise different tax considerations - primarily around how the corporation later repays the shareholder, and whether any interest charged is deductible to the corporation and taxable to the shareholder.

Q: My spouse received money from my corporation. Does that count as my shareholder loan?

Potentially yes. Section 15(2) captures loans to a shareholder or a person connected to a shareholder. The income inclusion attaches to the shareholder (and not the connected person, unless the connected person is themselves a shareholder.

Q: How does the section 80.4 deemed interest benefit interact with the subsection 15(2) inclusion?

They are separate provisions and can apply to the same loan. If the loan stays within the subsection 15(2.6) window and is properly repaid, subsection 15(2) does not apply - but section 80.4 still creates a taxable benefit for each year the loan was interest-free or below the prescribed rate. If the loan is caught by subsection 15(2), the principal is included in income; subsequent repayments may then be deductible under paragraph 20(1)(j), but the interaction is mechanical and requires careful tracking.

Q: My accountant said we'd "deal with it at year-end." Is that fine?

Sometimes, but generally no. The risk is that the option set at year-end may be narrower than the option set six months earlier. Dividend declarations need cash, salary requires payroll setup and tax withholding, and the subsection 15(2.4) exceptions need documentation in place at the time of the loan. The owners who manage this best treat the shareholder loan account as a monthly conversation, not an annual one.

Shareholder loan exposure is one of the clearest signals that a business has outgrown its bookkeeping setup. If your loan account has been quietly growing, or you're not sure whether your current structure is creating risk, ConnectCPA provides the monthly financial oversight and controllership support that catches issues like this before they become reassessments. To learn more about our controllership services, book a complimentary session here.